TL;DR

You spent millions on performance marketing.

You optimized the KYC flow to under 2 minutes.

The user clicked "Submit." The account is open.

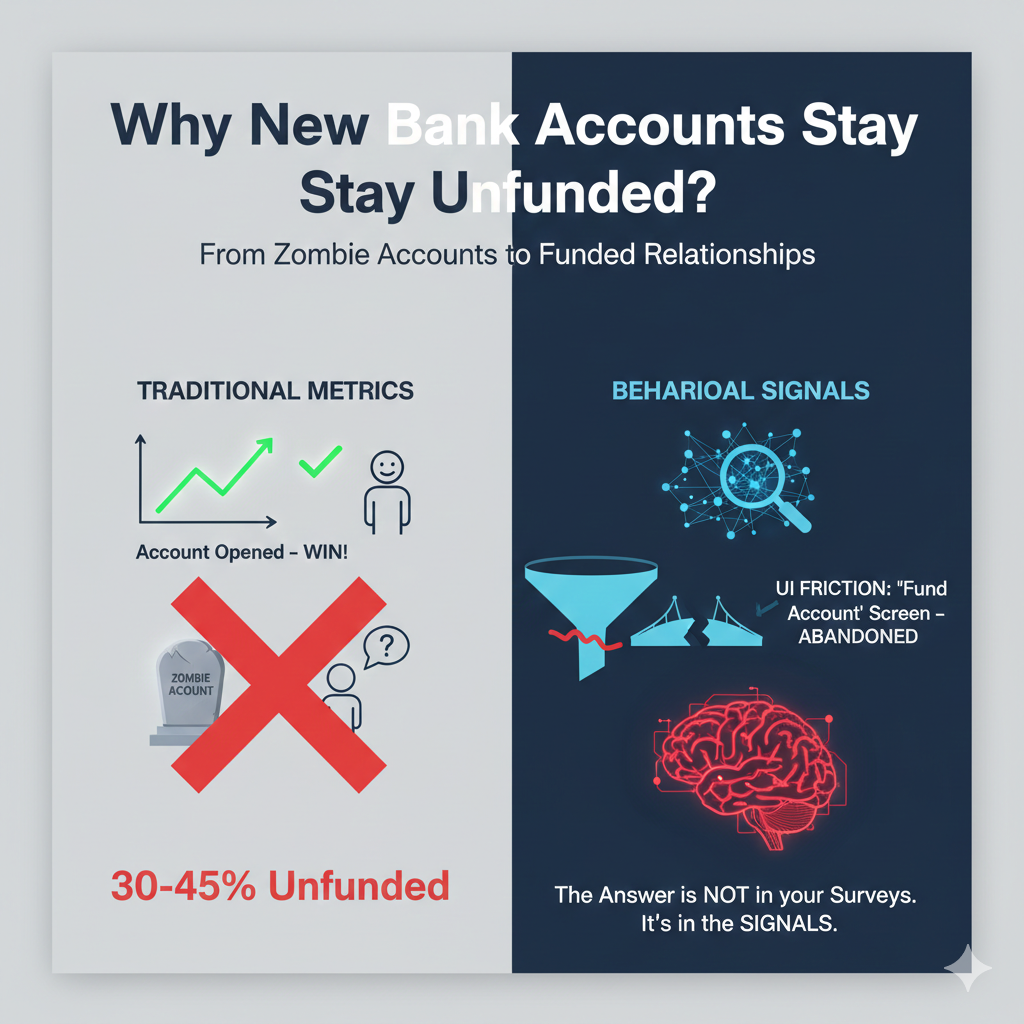

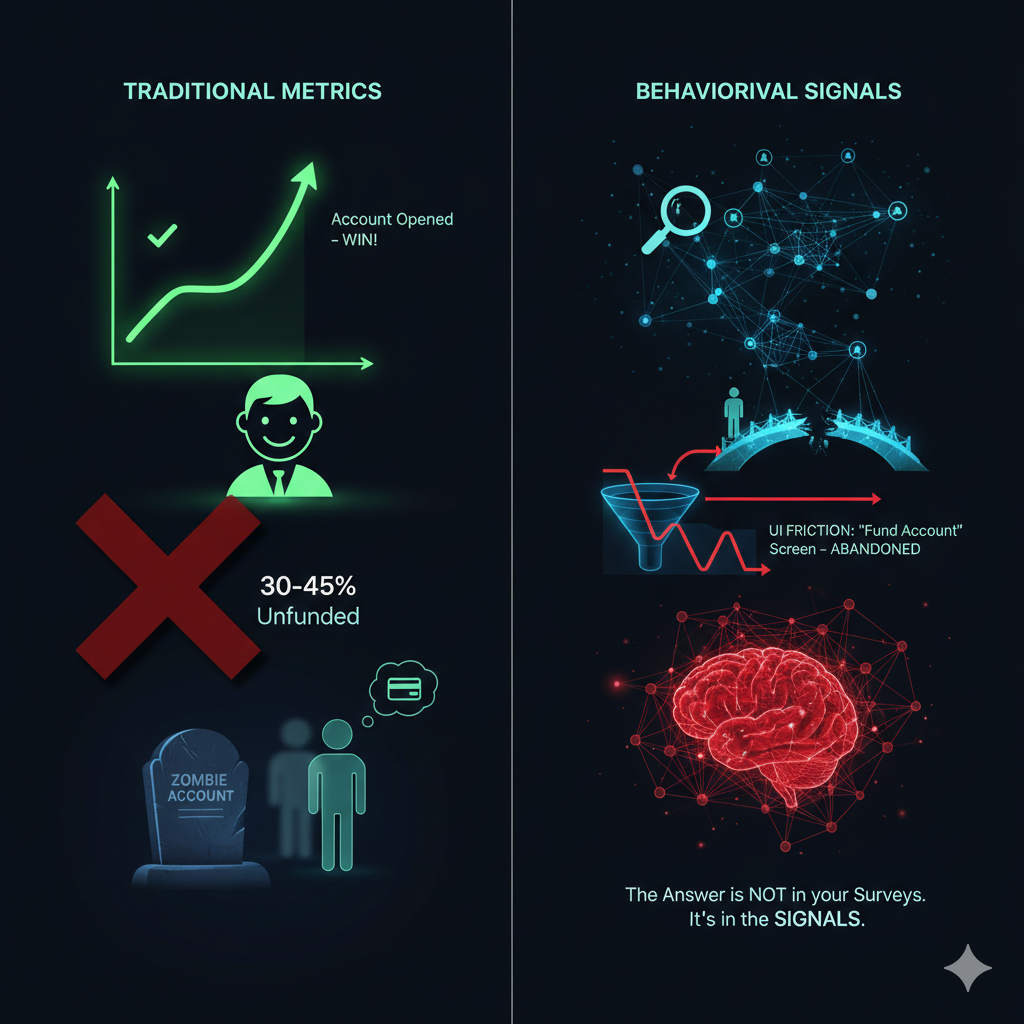

The dashboard marks it as a "Win."

But 30 days later, the balance is $0.00. This is the silent killer of retail banking profitability: the Unfunded Account.

As Shardendu Jha, Partner in Technology Consulting at EY, explained in recent research on digital customer onboarding, “Digital onboarding still often feels like a series of disconnected steps rather than a seamless journey. Banks may think they’ve ‘digitized’ onboarding, but until they truly streamline and intelligently automate the experience, customers will drop off because the process feels too long, confusing, or fragmented.” This highlights that the problem isn’t just account opening it’s a broken customer experience that fails to carry users through to first funding

This is the silent killer of retail banking profitability: the Unfunded Account.

According to recent 2026 data, 30-45% of newly opened accounts never receive an initial deposit.

In the industry, we call these "Zombie Accounts."

They are alive in your core banking system.

They consume compliance resources.

They inflate your acquisition metrics.

But they are dead on arrival.

For banking CX researchers and data science teams, this presents a paradox.

The customer had high enough intent to give you their Social Security Number and scan their ID.

So why did they stop at the finish line?

The answer isn't in your survey data.

It’s hidden in the behavioral signals in banking systems that most analytics teams are ignoring.

An unfunded account is not neutral; it is a liability.

Data from MX Technologies highlights that consumers who establish direct deposit within the first 30 days are 76% more likely to be digitally engaged after one year.

Conversely, those who miss this window usually churn.

If your journey analytics banking dashboard stops tracking at "Account Open," you are optimizing for vanity, not value.

You need to shift focus to "Time to First Funding."

Why does a customer open an account and then ghost you?

Traditional feedback loops (surveys) fail here because these customers don't stick around to answer them.

They just leave.

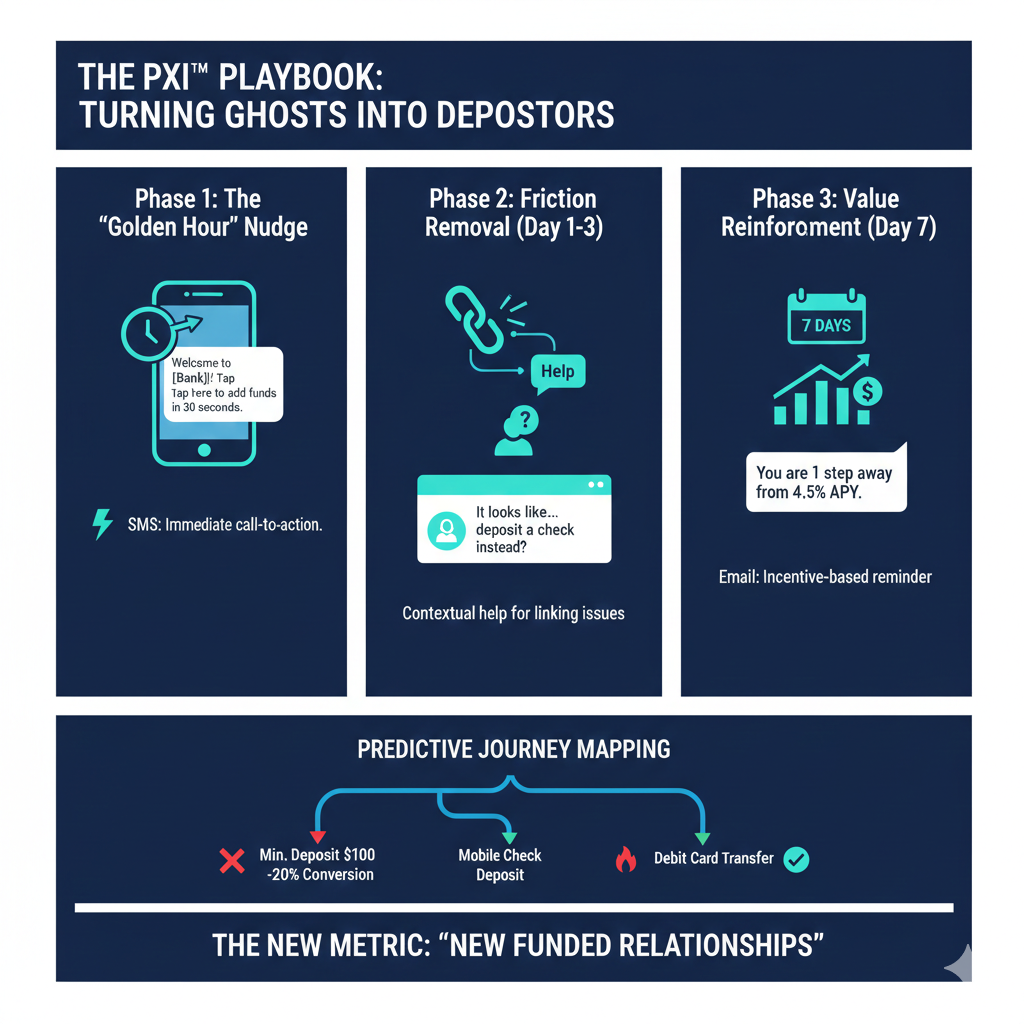

However, PXI (Predictive Experience Intelligence) - NUMR CXM’s proprietary model, can pick up the behavioral signals in banking platforms which showcase the "Digital Body Language" of these users.

We can categorize the "Unfunded" cohort into three specific risk profiles based on their customer inactivity triggers:

For data science & behavior analytics teams in retail banking, relying on monthly active users (MAU) is too slow.

You need low engagement indicators and banking metrics that fire in the first 24-48 hours.

By integrating these signals into journey analytics banking models, you can predict "Zombie" status with 85% accuracy within the first hour of opening.

To solve this, we must move from "Passive Reporting" to "Active Intervention."

This is the PXI™ approach to curing unfunded accounts.

The first hour after opening is critical.

If behavioral signals in banking show the user opened the account but closed the session without funding:

If the user returns but struggles:

If the account remains $0:

Advanced teams are now using predictive journey mapping to simulate these outcomes before they happen.

By analyzing historical user engagement metrics CX, you can identify which "Funding Paths" lead to the highest abandonment.

Use this data to re-engineer the UI, making the path of least resistance the default option for new users.

Acquiring a customer who doesn't fund is like buying a car and never putting gas in it.

It looks good in the driveway, but it won't take you anywhere.

The era of celebrating "New Accounts Opened" is over.

The new metric is "New Funded Relationships."

By leveraging behavioral signals in banking, you can see the friction that creates zombies.

You can see the hesitation.

And most importantly, you can fix it.

Don't let your marketing budget die in an empty vault.

Q: What are the most predictive behavioral signals in banking for funding churn?

A: "Time on Funding Screen" and "Error Message Frequency" are top indicators. If a user spends >2 minutes on the funding selection screen without action, or triggers >2 error messages during linkage, the probability of them leaving the account unfunded increases by 60%.

Q: How do we distinguish between 'low interest' and 'high friction' customers?

A: Journey analytics banking tools can differentiate. 'Low interest' users typically open the account and never log in again. 'High friction' users log in, attempt a task (like linking a bank), fail, and then leave. The latter group is highly salvageable with the right intervention.

Q: What are common customer inactivity triggers during onboarding?

A: The most common triggers include: delayed micro-deposits (waiting 1-2 days), unclear limits on mobile check deposits, and aggressive immediate minimum balance requirements. Detecting these low engagement indicators banking allows for rapid UI adjustments.

Q: Can we use these signals for compliance?

A: Yes. Behavioral signals in banking can also detect fraud (e.g., bot-like speed in form filling or pasting data into fields). However, for CX, the focus is on distinguishing legitimate users struggling with UX from actual bad actors.

Q: How does this impact user engagement metrics CX reporting?

A: It shifts the reporting from "Volume" to "Velocity." Instead of reporting "10,000 new accounts," you report "Average Time to First Funding." Reducing this time metric is directly correlated with higher Customer Lifetime Value (CLV).

How many millions in potential deposits are sitting in your "Unfunded" bucket right now?

PXI doesn't just count them; it wakes them up.

Recover your unfunded accounts with NUMR.

Book a strategy session with our CX architects to see how Predictive Experience Intelligence (PXI™) detects the friction stopping your deposits and automates the fix.

.png)

.png)

.png)