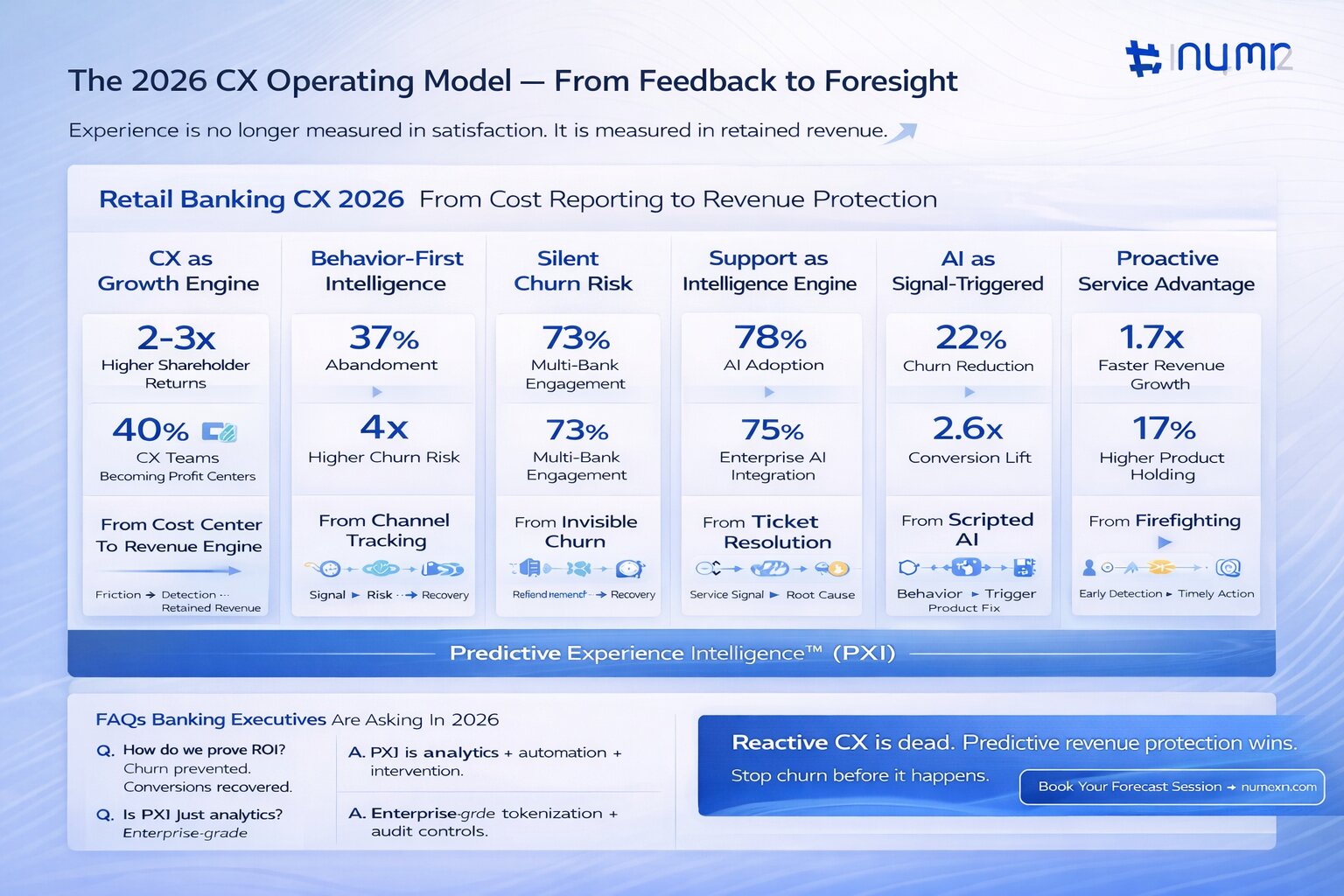

In 2025, retail banking customer experience is no longer a back-office metric; it is a revenue engine under boardroom scrutiny. Banks that rely on surveys and NPS are falling behind, while leaders are adopting the Predictive Experience Intelligence (PXI) model by NUMR CXM to detect risk, forecast churn, and recover lost revenue before it disappears. These are the top trends shaping the future of banking CX.

For decades, CX in retail banking was managed as a service function - measured in complaints resolved and NPS points earned. That era is over. In 2025, CX has become a strategic lever for profitability and is emerging as a business-critical function essential for preventing revenue leakage, reducing customer churn, and maximizing lifetime value.

As noted by McKinsey & Company,

“Companies that lead in customer experience grow revenues faster and deliver significantly higher shareholder returns than laggards.”

This shift explains why CX has moved from operational reporting into executive strategy discussions. Banking leaders are no longer asking whether experience matters; they are asking how much revenue is currently hidden inside experience friction.

This strategic pivot is being driven by two key forces:

The goal is to stop treating customer service as a cost to be minimized and to start treating it as a strategic asset for growth.

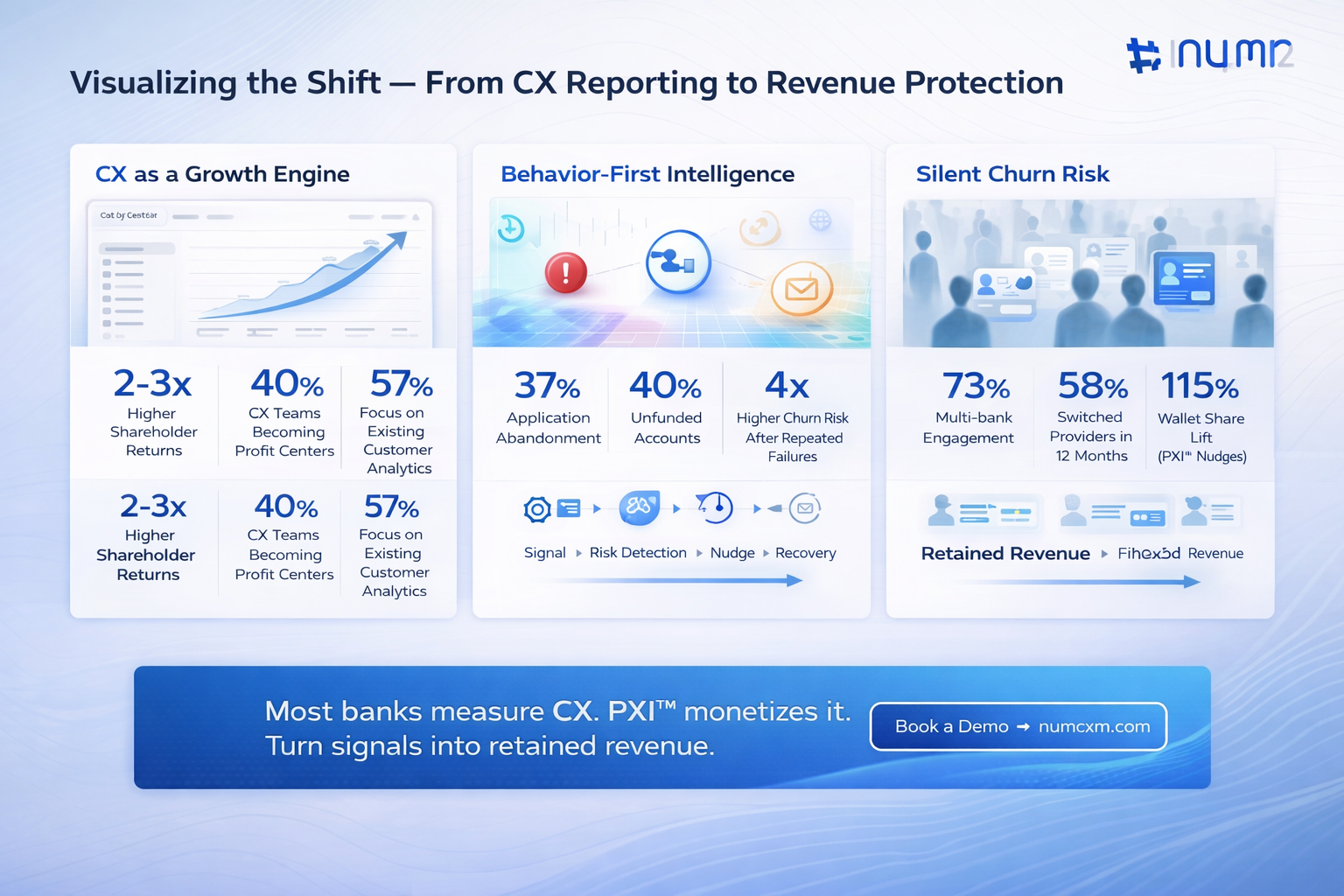

A significant shift is occurring toward deepening established relationships, with data analytics applications for existing customers having increased from 52% to 57% as a primary focus.

Simultaneously, customer engagement strategies have gained prominence, rising from 17% to 21% as a top priority for banking leaders.

Executives now demand that CX leaders quantify revenue at risk. They want to know:

According to Gartner,

“Customer experience leaders must demonstrate measurable business outcomes, not satisfaction scores alone.”

This pressure is reshaping CX operating models across retail banking. Experience teams are increasingly evaluated using financial KPIs such as retained deposits, activation rates, and prevented churn rather than traditional survey benchmarks.

Banks that answer these questions with precision are winning. McKinsey finds that financial institutions tying CX directly to growth achieve 2–3x higher total shareholder returns. And Gartner projects that by 2025, 40% of CX organizations will operate as profit centers, accountable for outcomes like churn reduction and conversion recovery.

The takeaway: CX leaders must stop reporting “satisfaction” and start reporting retained revenue. PXI makes that shift possible.

Traditional CX asked, “Which channel did the customer use?”

In 2026, that’s the wrong question. The right one is: “What was the customer doing right before they became frustrated?”

Consider the data:

A behavior-first approach surfaces these friction signals - failed logins, repeated app crashes, incomplete transactions; and acts on them. PXI platforms ingest these signals and generate micro-cohort alerts, enabling banks to intervene before frustration turns into attrition.

Instead of waiting for a complaint, banks can proactively send an RM nudge, trigger an agent callback, or guide the customer back into a successful journey.

This is a fundamental change from simply deflecting calls to intervening upstream to protect the customer relationship. The core of this trend is the use of behavioral insights to deliver timely, context-aware assistance.

Look for a growing focus on micro-cohort-based alerting and real-time sentiment modeling as banks become more adept at identifying these silent signals of frustration.

This is especially critical given the consumer paradox in 2026: while 42% of U.S. consumers prefer using a mobile app to manage their finances , 71% still say that in-person access is important and 68% say that phone support is essential.

The shift is profound: from reacting to complaints to intervening at the exact moment of risk.

Churn has always been a concern, but in 2026 the focus is on silent churn - customers who look active on paper but have disengaged in reality.

Examples include:

Silent churn poisons every downstream calculation - from cross-sell forecasts to lifetime value models. Banks might assume a customer is engaged when, in reality, the relationship is already over.

Research highlighted by The Financial Brand notes that many banks dramatically overestimate engagement because inactive customers still appear “active” in reporting dashboards. This illusion of engagement is precisely why silent churn has escalated from a CX issue to a CEO-level financial risk.

This is a pervasive issue, as 73% of customers now engage with multiple banks beyond their primary one, and 58% have purchased a financial service or product from a new provider in the last 12 months.

The PXI™ system addresses this by using behavioral cohorting to identify disengaged “ghosts.”

One bank using PXI™ nudges lifted wallet share by 115% simply by re-engaging dormant wealth with the customers who had opened but not funded accounts.

Silent churn is no longer a metric CX teams discuss in isolation - it’s a CEO and CFO-level concern tied directly to revenue reporting.

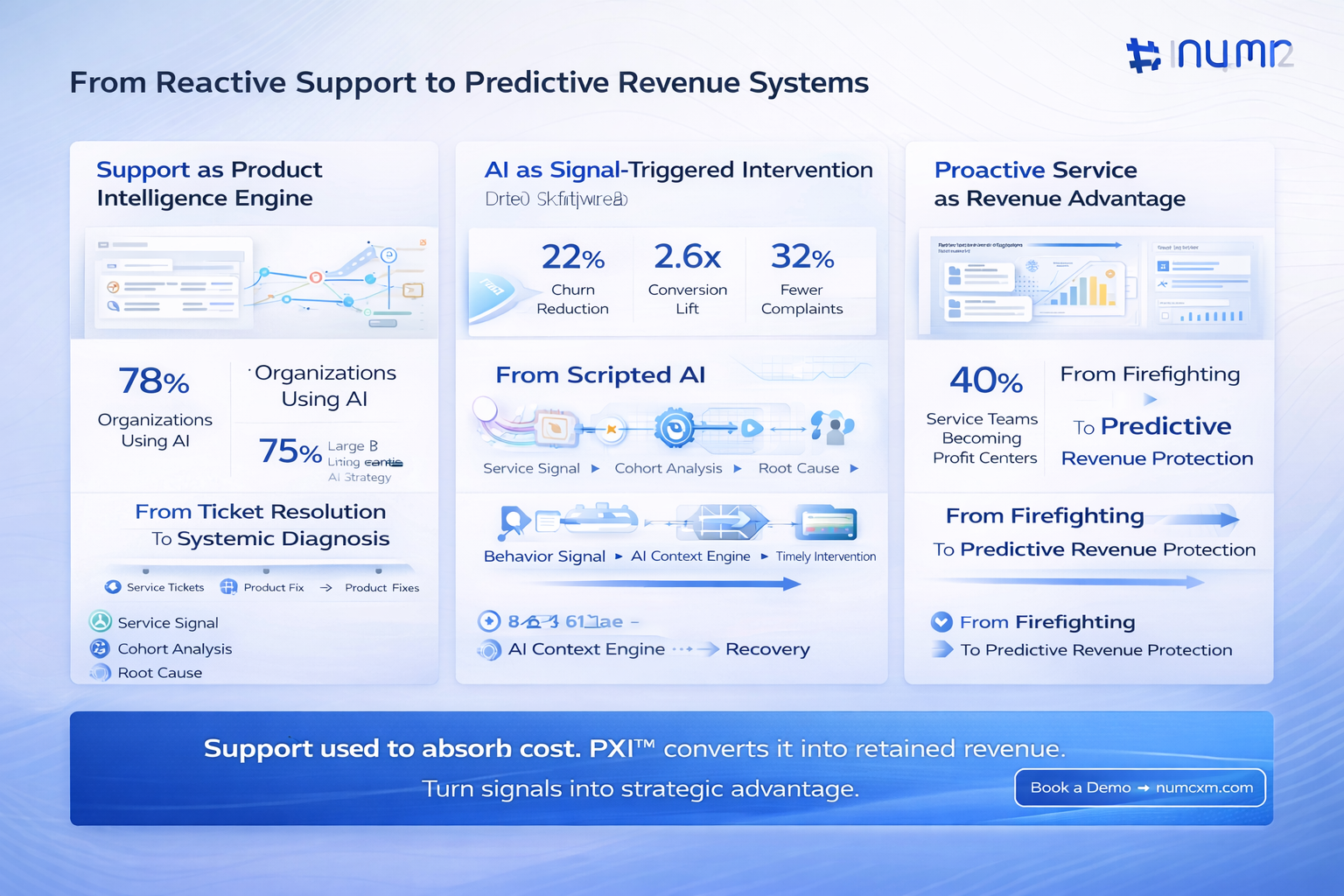

Support used to be where problems went to die. Today, leading banks are transforming it into the single most valuable intelligence engine for product and operations.

Every service ticket is a signal:

This feedback loop is increasingly AI-assisted, cohort-driven, and essential for fixing revenue leaks and improving product adoption at scale. This transformation is being driven by the maturation of AI, which is no longer a peripheral tool but a foundational utility.

In fact, 78% of organizations now use AI in at least one business function, and 75% of banks with over USD 100 billion in assets are expected to fully integrate AI strategies by the end of the year.

In 2026, PXI™ closes the loop by feeding these signals back into product, design, and ops teams in real time. Frontline service is no longer about damage control; it’s about systemic diagnosis and fix-at-source resolution.

For a VP of Retail Banking, this means service data is no longer a cost drag - it’s an asset that improves adoption, reduces churn, and drives profitability.

While AI chatbots are now ubiquitous, the leaders in 2026 are moving beyond simple keyword-based routing and are using behavioral signals to decide what to say, when to escalate, and how to route the customer to the best outcome.

This is a move from passive, scripted conversations to intelligent, proactive interventions. The imperative to adopt AI for efficiency is now inseparable from the need to use AI for security, with 67% of banking technology leaders actively piloting or in production with generative AI projects for cybersecurity.

We all know that banks have already deployed chatbots. But in 2026, the real differentiator isn’t AI for routing, it’s AI for signal-triggered action.

Think about these scenarios:

This is where PXI™ shines - not replacing agents, but making them appear in the right moment, in the right context, to the right customer.

The outcome? Banks see 22% churn reduction, 2.6x conversion lift, and 32% fewer complaints when PXI-driven interventions replace generic, script-based responses.

The ultimate goal of these trends is to shift customer service from reactive firefighting to predictive revenue protection. Banks with predictive support capabilities see measurable gains in retention, cross-sell, and profitability.

Gartner predicted that by the end of 2025, 40% of customer service organizations will become profit centers by adopting predictive service and outcome-based performance metrics.

This shift is particularly impactful as banks with the highest customer advocacy scores achieve 1.7 times faster revenue growth, and these advocates hold, on average, 17% more products with their primary bank.

The leaders in 2026 will have the tools to:

This shift turns every customer interaction into a strategic opportunity to build loyalty and drive financial outcomes.

Q1. What tools do we need to adopt these CX trends?

Q2. How do we prove ROI from these CX changes?

Q3. Is PXI just another analytics tool?

Q4. How secure is PXI™ for sensitive banking data?

In 2026, reactive CX is dead. The future belongs to banks that forecast friction, prevent silent churn, and convert signals into revenue protection.

PXI™ is not just a technology shift - it’s a category shift. It redefines customer experience as foresight, not feedback.

Book your Forecast Session with NUMR and discover how to stop churn before it happens.

.png)

.png)

.png)