Segmenting Customers for Better Banking Product Adoption Outcomes

TL;DR

Banks have mastered digital activation (83% of US adults are active), but product adoption remains stagnant because teams rely on static, demographic profiles.

Knowing "Who" the customer is (Age, Income, Geo) tells you nothing about "How" they struggle.

Predictive Experience Intelligence (PXI) replaces static segments with Dynamic Risk Pods—micro-clusters defined by behavior, friction, and revenue threat.

This guide provides the PXI Segmentation Framework to turn analytics into an automated adoption engine.

Introduction: Why Your Analytics Dashboard Is Lying

You’ve invested heavily in digital onboarding.

Your product teams shipped features faster than ever.

Your CX dashboards show "healthy" engagement on paper.

And yet adoption still stalls.

Across U.S. retail banking, this has become the "Silent Crisis" of 2025 that is infiltrating 2026: Strong Activation, Weak Sustained Usage.

Customers sign up, log in, and maybe complete one transaction.

Then they drift.

They don't adopt the bill pay feature. They don't set up recurring transfers. They don't move from "User" to "Advocate."

The problem isn’t your features. It’s your map.

Traditional segmentation tells you who the customer is but not how they adopt products, engage with features, or encounter friction.

As analysts at Forrester have observed, “Segmentation should not be about who the customer is, it should be about what the customer does. Behavioral segmentation, especially when powered by real-time signals and analytics, consistently outperforms demographic profiling for predicting engagement, retention, and product adoption.” This reflects a broader industry shift toward data-driven, experience-centric segmentation that directly correlates with usage and value realization rather than static traits.

Most banks are still segmenting customers for marketing efficiency (Who are they?), not for product adoption outcomes (What are they doing?).

Demographics are a vanity metric in product adoption.

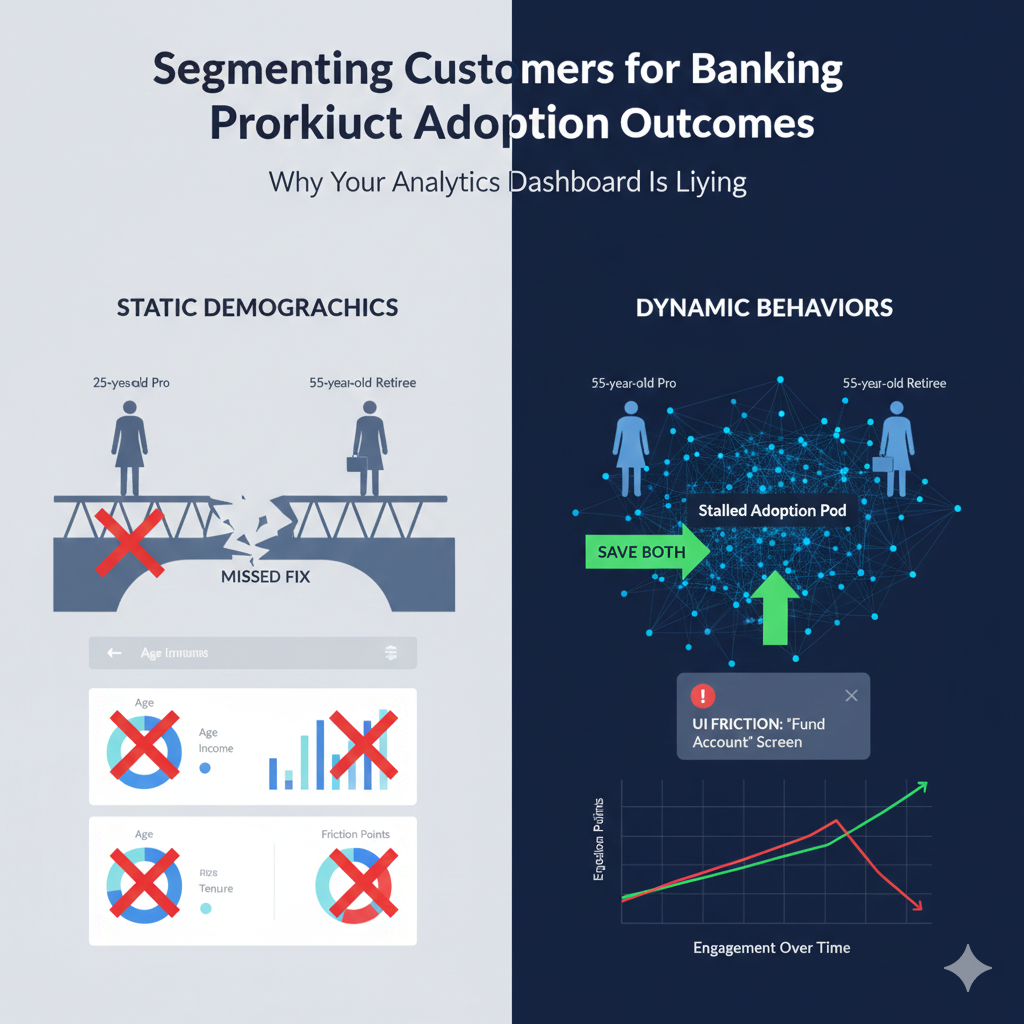

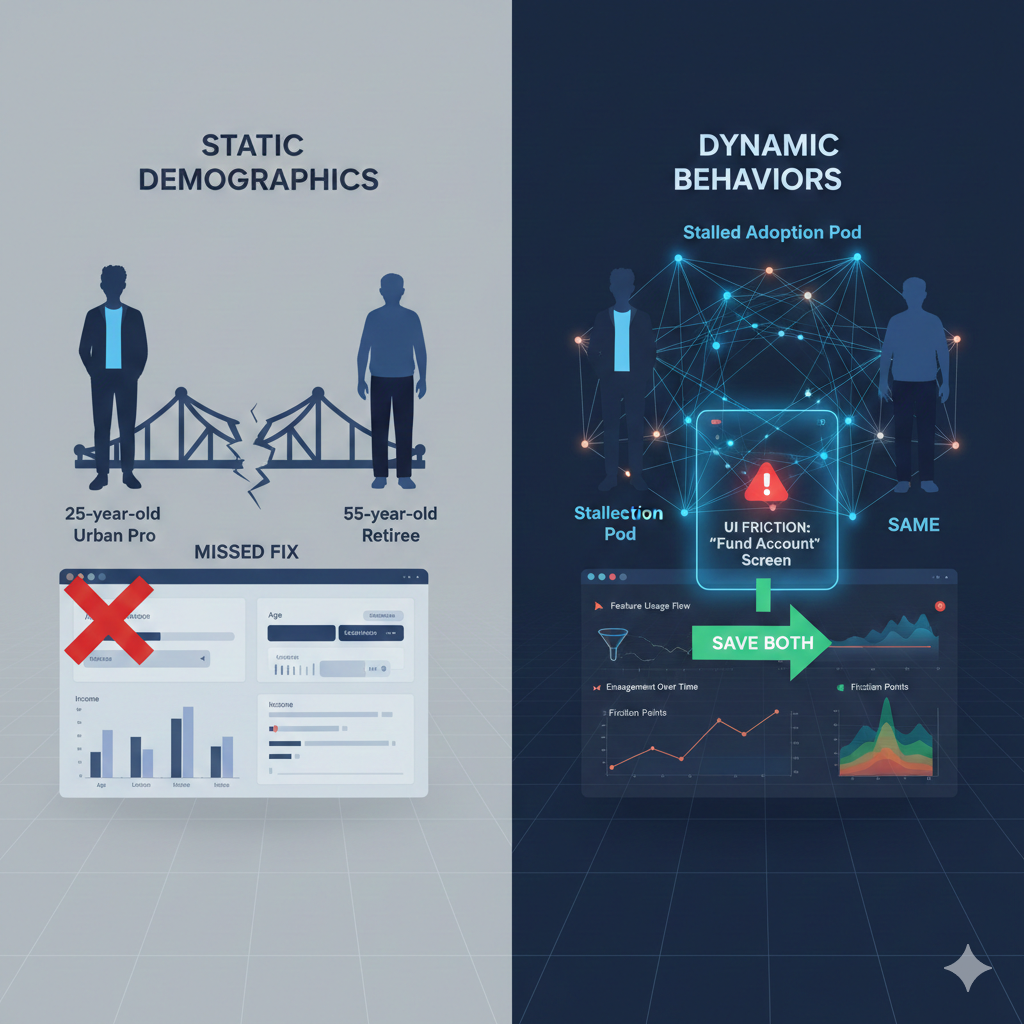

A 25-year-old urban professional and a 55-year-old retiree can belong to the exact same "Stalled Adoption Pod" if they both hit the same UI friction on the "Fund Account" screen.

If you treat them differently because of their age, you miss the fix.

If you treat them the same because of their behavior, you save them both.

Why Traditional Segmentation Fails Adoption

Most retail banks don’t struggle with data. They struggle with meaning.

You likely already segment by Age, Income, Tenure, or Account Type.

These segments are clean, familiar, and easy to explain to the Board.

But when adoption stalls, those segments stop being useful.

Who the customer is rarely explains how they behave.

1. The Demographic Blind Spot

The Stat: Digital banking has reached 83% adoption among U.S. adults. Nearly everyone is "digital."

The Reality:71% of customers aged 18–34 primarily manage finances digitally, yet usage depth varies wildly.

The PXI Insight: Two customers in the same "Gen Z High Earner" segment can have opposite values. One uses your budgeting tool daily (High Value). The other logs in only to check balances (High Risk). Demographics group them together; PXI separates them.

2. The "Static Segment" Trap

The Stat:75% of companies struggle with data silos, making it difficult to update segments as behavior changes.

The Consequence: A customer activates and gets labeled "Engaged." Three months later, their usage drops, but the label stays.

The PXI Insight: Value realization is not static. As Jocelyn Brown, Head of Customer Success at Hypercontext, notes: "Value realization is defined by the customer—and it is not static."

Behavioral segmentation is 3–5× more effective than demographic segmentation at predicting retention.

It’s time to stop building Profiles and start building Pods.

Pod (PXI Way): "High-Balance Users who failed to set up Auto-Pay twice in the last 7 days." (Predictive & Actionable)

When you segment by Pod, the "Next Best Action" becomes obvious. You don't send a newsletter; you fix the specific friction that created the Pod.

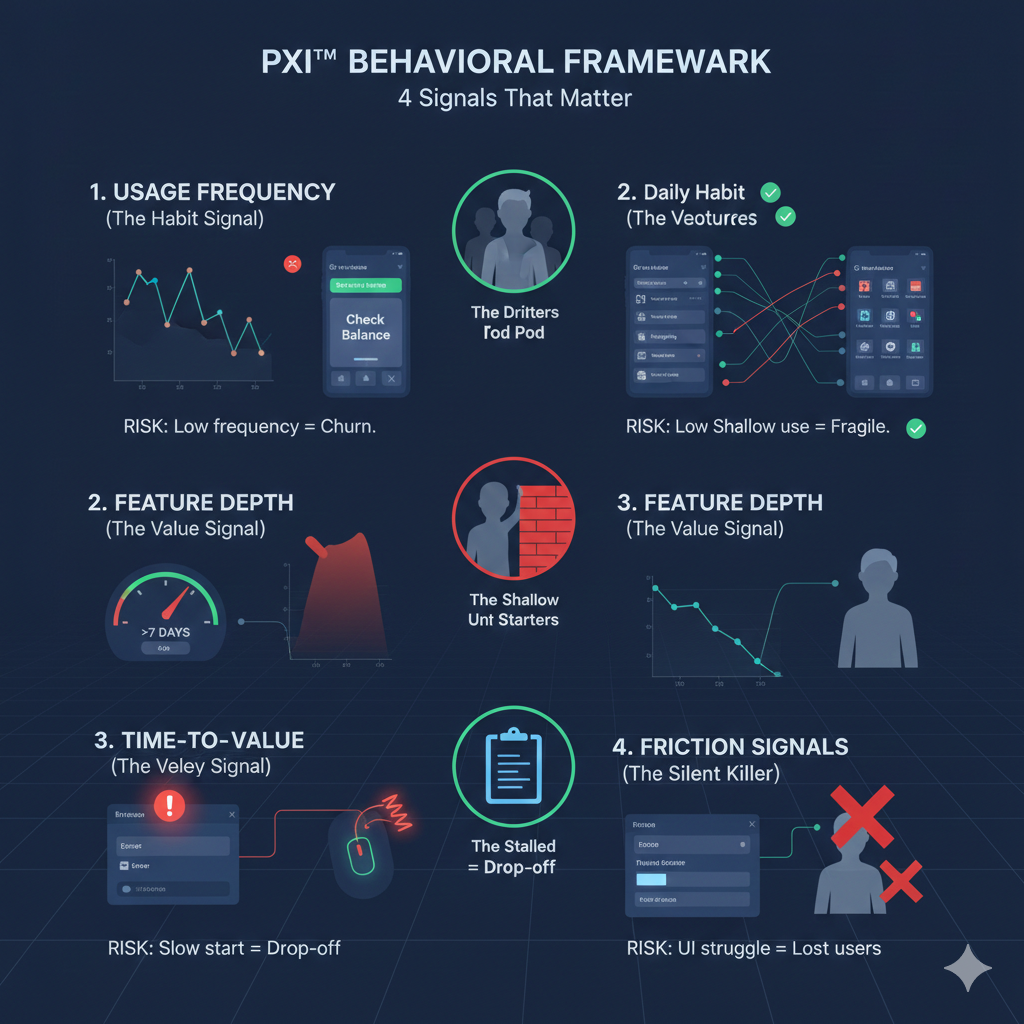

The PXI™ Behavioral Framework: 4 Signals That Matter

To operationalize this, stop tracking 50 metrics. Track the 4 Signals of Adoption.

1. Usage Frequency (The Habit Signal)

What it is: Not just logins, but unprompted return rate.

The PXI Signal: Does the user return naturally within 3 days, or only after a push notification?

The Risk: Low frequency in the first 30 days is the #1 predictor of Day 90 churn.

The Pod:"The Drifters." They log in sporadically. They haven't formed the neural pathway that connects your app to their financial anxiety.

2. Feature Depth (The Value Signal)

What it is: The breadth of features used vs. features available.

The PXI Signal: Are they using "Read-Only" features (Check Balance) or "Write" features (Bill Pay, Transfer)?

The Risk: "Read-Only" users are easily poached by competitors offering better rates. "Write" users are sticky.

The Pod:"The Shallow Adopters." They look active, but they are fragile. They haven't tasted the real value.

3. Time-to-Value (The Velocity Signal)

What it is: The speed at which a user completes their first meaningful action (e.g., funding an account).

The PXI Signal: If Time_to_Fund > 7 days, drop-off probability spikes by 40%.

The Pod:"The Stalled Starters." They have high intent but hit a wall.

4. Friction Signals (The Silent Killer)

What it is: The digital body language of struggle.

The PXI Signal: Rage clicks, scroll reversals, repeated error messages, or "clipboard usage" (copying an account number but never pasting it).

The Pod:"The Frustrated High-Intents." These are your most tragic losses. They wanted to adopt, but your UI stopped them.

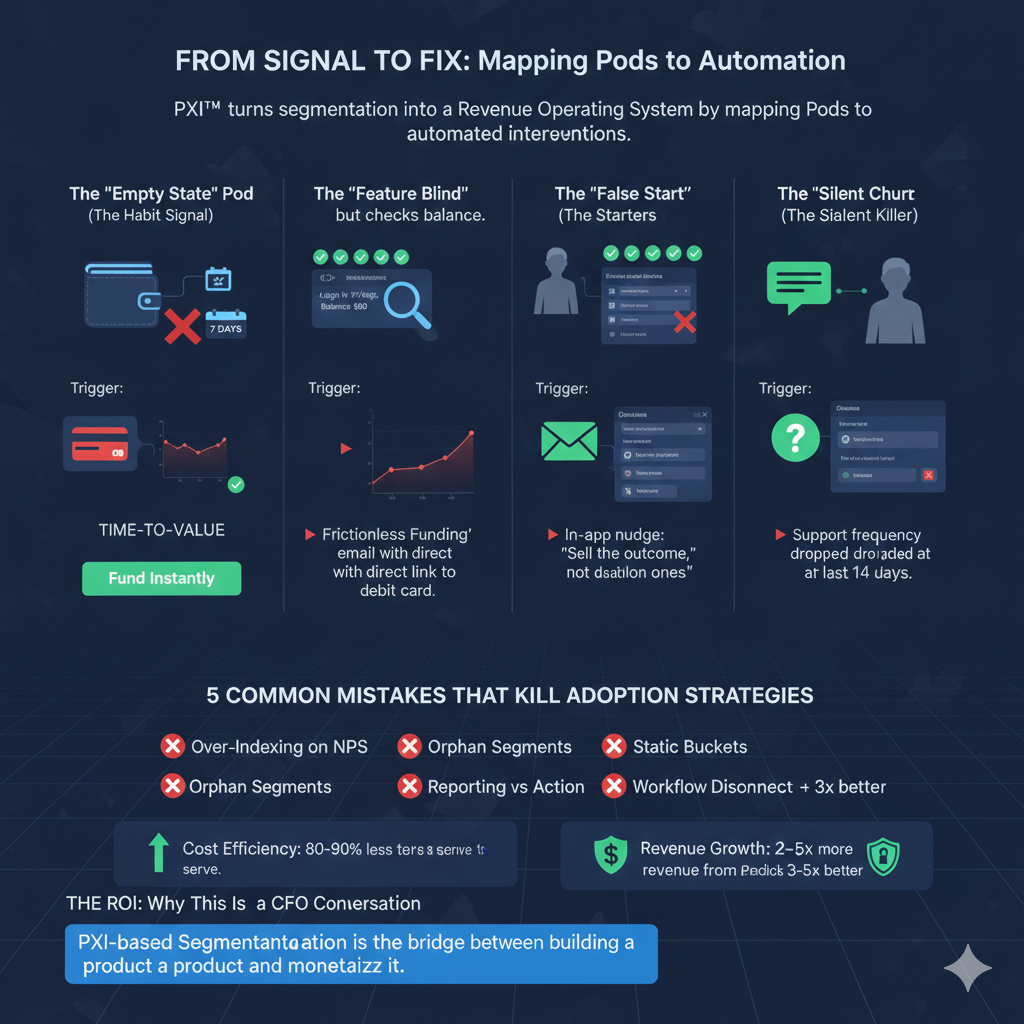

From Signal to Fix: Mapping Pods to Automation

Segmentation is useless if it lives in a slide deck.

PXI™ turns segmentation into a Revenue Operating System by mapping Pods to automated interventions.

PXI™ Pods, Signals & Interventions

The Pod (Segment)

The Signal (Behavior)

The PXI Intervention (Fix)

The "Empty State" Pod

Account open > 7 days, balance remains $0.

Trigger a “Frictionless Funding” email with a direct link to debit card funding, bypassing the micro-deposit wait.

The "Feature Blind" Pod

Logs in 5× per week but only checks balance.

In-app nudge: “Tired of checking? Set up a low-balance alert in 2 clicks.”

Sell the outcome, not the feature.

The "False Start" Pod

Started Bill Pay setup but abandoned at “Add Payee.”

Contextual guide: “Can’t find your provider? Here’s a list of common ones.”

The "Silent Churn" Pod

Usage frequency dropped by 50% in the last 14 days.

Proactive support outreach or a targeted retention offer before usage hits zero.

5 Common Mistakes That Kill Adoption Strategies

Even with data, banks fail because they treat segmentation as an analytics output, not an adoption operating system.

Over-Indexing on NPS: NPS tells you how they feel. Adoption tells you what they do. PXI trusts behavior over sentiment.

Orphan Segments: Creating segments that no team owns. If "The Stalled Starter" pod doesn't have a specific Product Owner, it will never shrink.

Static Buckets: Treating segmentation as a one-time project. Pods are living organisms; they grow and shrink daily.

Reporting vs. Action: Optimizing segments for dashboards instead of decisions. If a segment doesn't answer "What do we do next?", delete it.

Workflow Disconnect: Keeping segmentation out of the tools teams actually use (CRM, Support Desk). PXI embeds the Pod tag directly into the agent's view.

The ROI: Why This Is a CFO Conversation

This isn't just about "better UX." This is about P&L defense.

Cost Efficiency: Digital-habitual customers cost 80-90% less to serve than branch-dependent ones.

Revenue Growth: Deep adopters (3+ features) generate 2x to 5x more revenue.

Retention: Behavioral segmentation predicts churn 3-5x better than demographics.

The Bottom Line:

Strong onboarding does not guarantee adoption.

Great features do not guarantee usage.

PXI-based Segmentation is the bridge between building a product and monetizing it.

FAQ: PXI & Behavioral Segmentation

Q: How is PXI segmentation different from traditional RFM (Recency, Frequency, Monetary) analysis?

A: RFM is backward-looking (what they did). PXI is predictive (what they will do). PXI analyzes micro-signals (like hesitation on a screen) to predict the risk of drop-off before the transaction data even exists.

Q: Do we need to replace our existing marketing personas?

A: No. Keep personas for acquisition brand messaging. Use PXI Pods for post-acquisition product adoption and retention. They serve different masters: Marketing vs. Product/Revenue.

Q: Can this approach work across multiple banking products?

A: Yes. It is most effective there. PXI identifies "Cross-Pollination" Pods - e.g., Checking customers who behave exactly like Credit Card adopters but haven't applied yet.

Q: Who should own this segmentation?

A: Shared ownership is non-negotiable. CX owns the signals. The product owns the fix. Ops owns the recovery. If it sits in a silo, it fails.

Q: How fast can we see results?

A: Unlike brand campaigns, behavioral interventions work instantly. Fixing a friction point for a "Stalled Pod" can lift conversion in 24-48 hours.

Next Steps: Audit Your Adoption Gaps

Do you know which "Pod" is leaking the most revenue right now?

It’s not the one screaming on social media. It’s the one suffering in silence.

.png)

.png)

.png)