TL;DR

You spend $500+ in customer acquisition costs (CAC) to acquire a new premium cardholder.

You offer 60,000 bonus points if they spend $4,000 in the first three months.

They hit the spend. They get the points.

And then... silence.

The transaction volume drops to zero. The card is removed from their digital wallet.

Six months later, they eventually close the account.

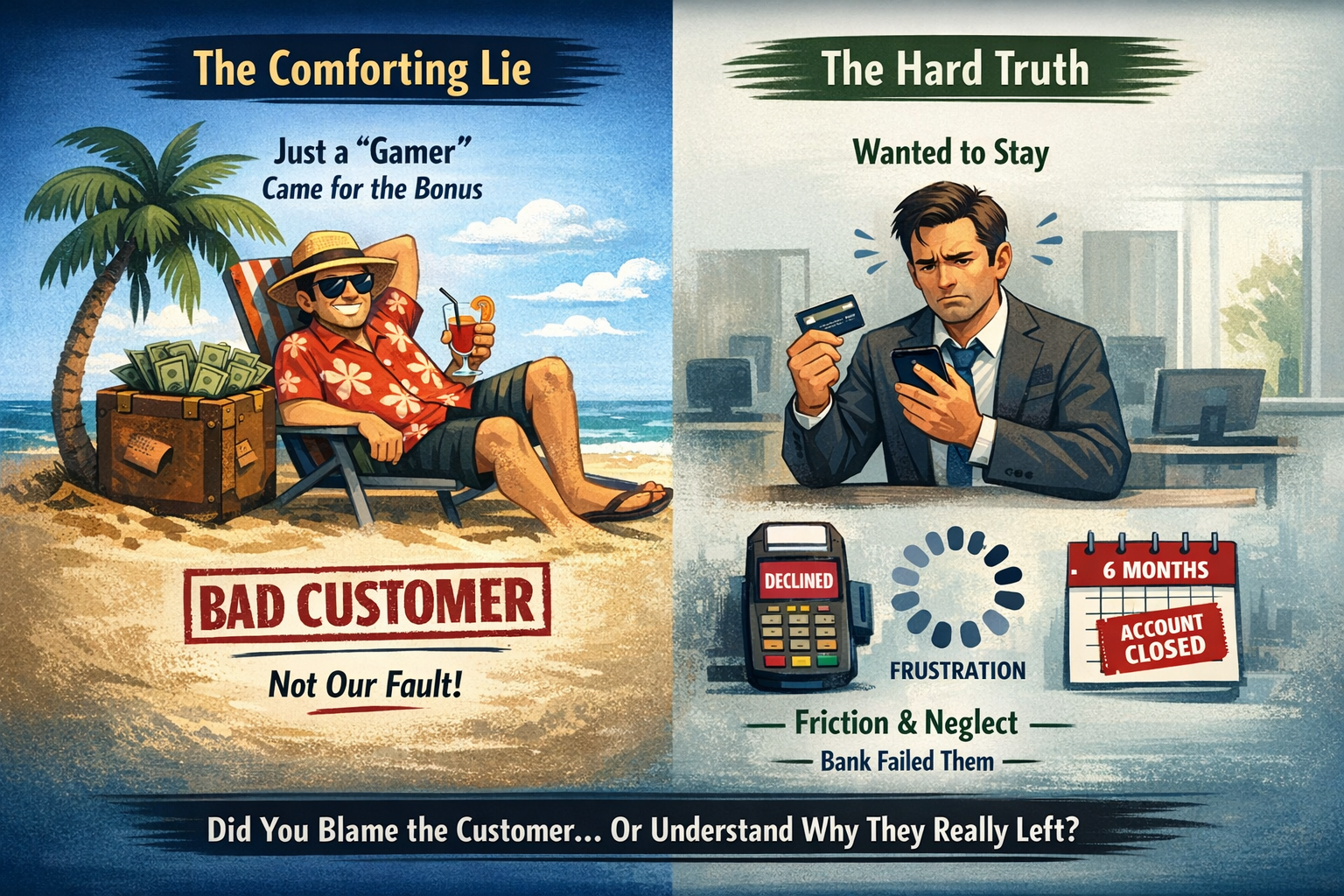

Most card portfolio managers and CX leaders write this off as "bad quality acquisition."

They label the customer a "gamer"- someone who just came for the bonus.

It’s a comforting lie.

It absolves the bank of responsibility.

But it is a lie that is costing you millions in customer value measurement banking.

The contrarian truth that should actually make you worried?

Most "gamers" are actually high-intent customers who wanted to stay.

They didn't leave because they got the bonus.

They left because you failed to migrate them from "incentivized spend" to "habitual spend."

You measured their transaction volume.

But you missed the friction that killed their loyalty.

The following sections show the statistical evidence that the post-promo drop-off in credit card usage is something real that bankers need to combat if they wish to improve their ROI.

Post-promotional drop-off manifests in multiple quantifiable dimensions. Capgemini's World Retail Banking Report 2025 found that when banks target 100 prospective new cardholders, only 9% successfully convert to customers. However, the challenge extends beyond acquisition: among those who do open new cards, satisfaction levels are markedly low. Only 26% of new cardholders report being satisfied with their card experience, while 50% remain indifferent and 24% report outright dissatisfaction.

This distribution with three-quarters of the customer base (74%) being either indifferent or dissatisfied - indicates that post-acquisition engagement strategies are substantially failing to deliver value beyond the promotional period.

The post-promotional period creates acute flight risk for new card issuers. Capgemini's research quantifies this risk explicitly: 74% of cardholders are identified as "potential flight risks" - consumers who have demonstrated receptiveness to switching to alternative card products after the promotional period concludes.

This statistic is particularly significant when combined with the earlier finding that only 9% of prospects convert to customers in the first place: the institutional challenge is not merely acquiring customers but retaining them once promotional incentives expire.

Broader loyalty program data illuminates the post-promotional engagement challenge. The Boston Consulting Group's 2025 Global Loyalty Report found that while consumer participation in loyalty programs has increased, the underlying strength of these relationships has deteriorated significantly[6]. Engagement metrics declined 10% among US consumers since 2022, and more critically, loyalty - measured as the degree to which consumers would consider alternative brands - declined by twice that amount at 20% below 2022 levels.

Credit card and streaming media programs experienced the lowest declines among loyalty categories, yet still showed meaningful deterioration, suggesting that even reward-focused mechanisms are failing to maintain engagement post-promotion.

Canadian credit card payment behavior provides direct evidence of post-promotional usage decline. According to FICO's Canada Bankcard Industry Benchmarking data for Q2 2025, payment rates (reflecting the proportion of monthly balances paid in full) declined substantially from historical levels:

· Mid-2023 baseline: 55% payment rate

· Early 2024: Sharp decline to 48-49% during Q1

· Mid-2025: Stabilization at 52-53% payment rate[7]

This 2-3 percentage point permanent decline from mid-2023 levels represents a structural shift in consumer behavior, not temporary seasonality. FICO analysts interpret this trend as consumers "prioritizing liquidity over debt reduction" - a pattern consistent with post-promotional cardholders reducing engagement and carrying balances rather than using the card for active spending.

Notably, this payment rate decline began in early 2024, approximately 12-18 months after the large cohort of new card issuances in late 2022 and early 2023 would have entered their post-promotional period. The timing alignment suggests causation between new card onboarding and subsequent payment behavior deterioration.

The Federal Reserve's analysis of recently issued credit card accounts provides another metric for post-promotional usage decline. While initial research by the Consumer Financial Protection Bureau suggested that accounts opened in 2022-2023 entered delinquency faster than pre-pandemic accounts, updated Federal Reserve Y-14M data indicates this was temporary.

More significantly, the research reveals that accounts opened in 2022 and 2023 showed the highest propensity to become delinquent within their first year of issuance: nearly 6% of 2022-vintage accounts became delinquent within 12 months of origination, compared to just over 4% for 2019-vintage accounts.

This 50% increase in first-year delinquencies among recent vintages correlates with promotional mechanics: cardholders who default in the first year are, by definition, post-promotional users, as most sign-up bonuses have 3-6 month spend requirements. The concentration of early delinquencies suggests that promotional offers may be attracting marginal credit quality customers who rapidly exhaust the promotional value and subsequently default rather than developing long-term usage patterns.

Till now it is evident that the math of credit card promo drop-off is brutal.

Acquiring a new customer is consistently 5 to 25 times more expensive than retaining an existing one.

Yet, many banks see annual credit card churn rates hover between 15-20%, with a massive spike occurring immediately after the introductory offer ends.

When a customer ghosts you after the promo, you haven't just lost a user.

You have lost:

A mere 5% increase in customer retention can boost profits by a staggering 25% to 95%.

So why are product adoption benchmarks in banking still focused on "new accounts opened" rather than "accounts habituated"?

Because CX performance metrics in banking are looking at the wrong things.

You are likely tracking:

Here is the problem.

A customer can spend $4,000 and still be completely unattached to your bank.

They might be "Active" in your CRM, but "Dormant" in their behavior.

This gap between reported activity and real engagement is a well-documented failure of customer experience measurement in retail banking. As Capgemini’s Global Banking Industry Leader Gareth Wilson notes, “At a time where convenience and personalization dictate customer expectations, banks need to invest in the end-to-end customer journey from onboarding to loyalty to mitigate the risk of losing primacy as the customer’s preferred banking partner.”

This is precisely where traditional metrics fall short.

And NPS?

Your "gamer" might give you a 10/10 because they loved the free flight they just booked with your points.

Then they churn the next day.

NPS is a lagging indicator.

It tells you how they felt about the reward.

It doesn't tell you if they faced friction adding your card to Apple Pay.

It doesn't tell you if they experienced a false decline, which causes more than one-third of consumers to abandon their card immediately.

It doesn't measure credit card activation analytics - the micro-steps that create stickiness.

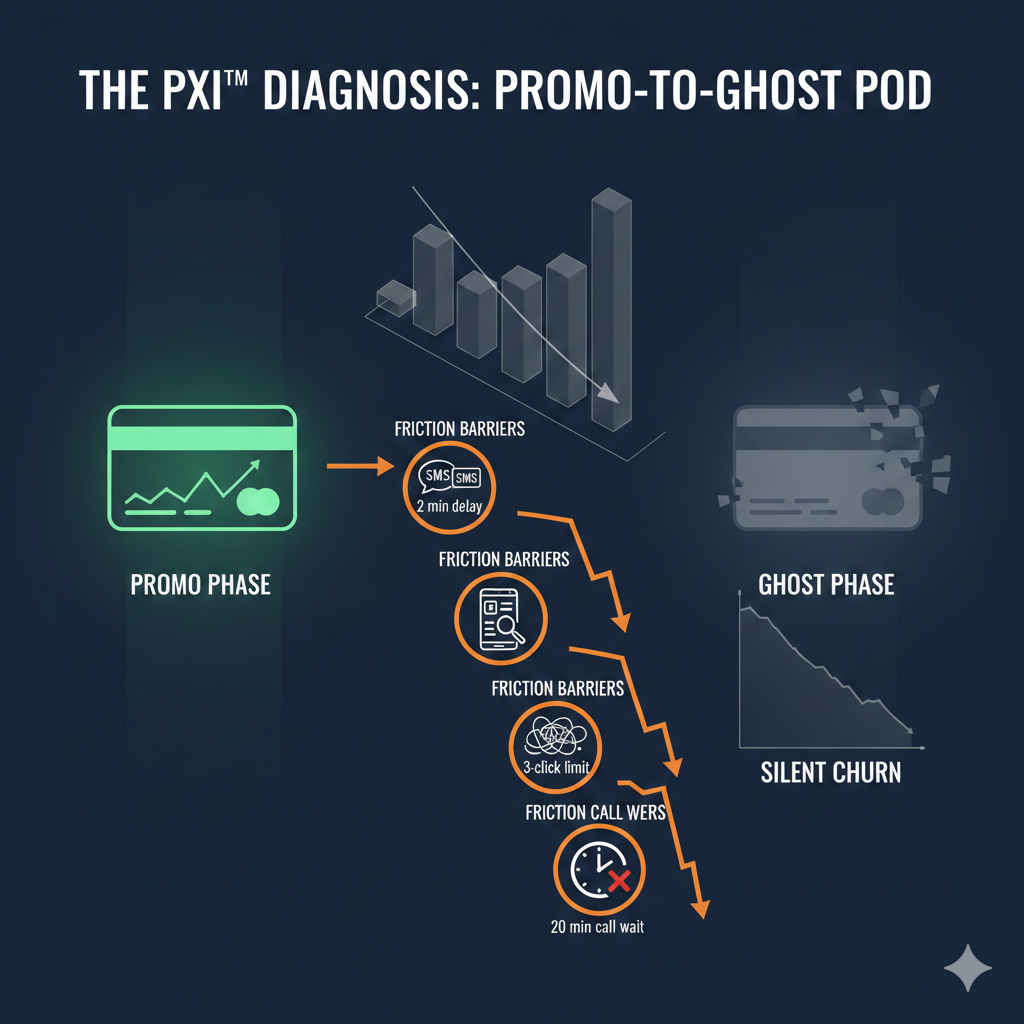

You need to shift from CX adoption measurement (reactive) to Predictive Experience Intelligence (proactive).

NUMR’s PXI™ framework doesn't look at "average users."

It clusters users into Pods - micro-cohorts with shared friction and revenue risk.

One of the most dangerous pods we see in promo usage analysis in banking is the "High Spend, Low Breadth" Pod.

The Signal:

The Risk:

This is not a loyal customer. This is a transactional user.

Once the incentive is gone, the transaction driver is gone.

This is an early drop-off indicator of credit card usage screaming at you.

The Reason:

PXI often finds that these users tried to do more but hit friction.

They didn't leave because they are "gamers."

They left because you made it hard to stay.

To stop promo spender churn in banking, you must intervene during the promo period.

You cannot wait for day 91. You must act on day 30.

Here is how CX consultants and ROI strategists use PXI™ to fix this:

Signal: Customer has spent $2,000 but has 0 recurring merchants.

Action: Trigger a personalized push notification or email: "Add us to your Netflix or Spotify account and get 500 extra points."

PXI Logic: One recurring bill reduces churn probability significantly. With recurring payments models showing reduced CAC and higher CLV, you are buying habituation, not just volume.

Signal: Customer added card to Google Pay but hasn't used it for 14 days.

Action: In-app prompt: "Trouble using your card with Google Pay? Here is a 1-tap guide."

PXI Logic: Digital onboarding optimization isn't just about signup. It's about usage friction. With digital banking apps seeing a ~30% drop-off in retention within the first 30 days, if they don't tap now, they won't stick later.

Signal: Spend decay models show a 20% week-over-week drop in transaction frequency, even if total volume is high.

Action: Alert the Relationship Manager (for high-value clients) or trigger an automated retention offer before they hit zero.

PXI Logic: Catch the spend decay while the card is still in their pocket. Silent churn is dangerous because it often goes unnoticed until the customer is gone.

This is where we talk about product adoption ROI in banking.

This is not "soft" CX. This is P&L defense.

By using CX journey analytics in banking to identify and fix these friction points, you change the unit economics of your portfolio.

The Calculation:

ROI of digital CX investments is not about surveys.

It is about saving the customers you already paid to acquire.

It is about proving that post-incentive customer behavior in credit cards can be engineered, not just observed.

If you are a research analyst or benchmarking consultant, you need to know what "good" looks like in 2026.

Your bank is likely running a factory that manufactures churn.

You pay to bring them in. You pay to incentivize them. And then you watch them leave because you didn't manage the customer retention in credit cards effectively.

Credit card retention strategy is not about better rewards.

Everyone has rewards.

Retention is about frictionless habituation.

It is about using customer behavior prediction to see the ghosting before it happens.

Don't let your "gamers" win.

Turn them into customers.

Q: What are the key CX performance metrics in banking for 2026?

A: Beyond NPS, leaders are tracking Customer Lifetime Value (CLV), Cost-to-Serve, and Retention Rate. Specifically, tracking the average adoption rate in banking products (like bill pay or mobile deposit) is a leading indicator of long-term loyalty.

Q: How does churn prediction differ from behavioral analytics?

A: Behavioral analytics in retail banking explains what happened (descriptive). Churn prediction models use that data to forecast what will happen (predictive). PXI combines both: it uses behavioral signals (like early drop-off indicators in credit card usage) to predict risk and trigger an automated fix.

Q: What is the average credit card churn rate?

A: Industry benchmarks place annual credit card churn between 15-20%. However, promo spender churn in banking can be significantly higher (40%+) if habituation strategies aren't deployed during the first 90 days.

Q: How can we measure the ROI of journey analytics?

A: You measure journey analytics ROI by linking specific fixes to retained revenue. For example, if credit card activation analytics identifies a friction point in the app, and fixing it increases activation by 10%, the product adoption ROI in banking is the lifetime value of those additional active customers minus the cost of the fix.

Q: What are the most critical banking customer engagement metrics?

A: Look for "Breath of Usage" (number of different transaction categories), "Digital Intensity" (login frequency + feature usage), and "Bill Pay Penetration." These banking CX KPIs correlate much more strongly with retention than simple spend volume.

Q: What tools are best for this?

A: You need CX intelligence tools that go beyond survey data. Predictive analytics for banks requires a platform like PXI that can ingest real-time behavioral signals, score customer activity (via customer activity scoring in banking), and automate interventions.

Stop guessing why your high-spend customers are vanishing.

PXI detects the friction hidden in your promo cohorts before they churn.

Book your Strategy Session with our CX architects at NUMR.

Witness how the Predictive Experience Intelligence (PXI™) framework can identify your "Promo-to-Ghost" pods and quantify the exact revenue you can recover in real-time.

.png)

.png)

.png)