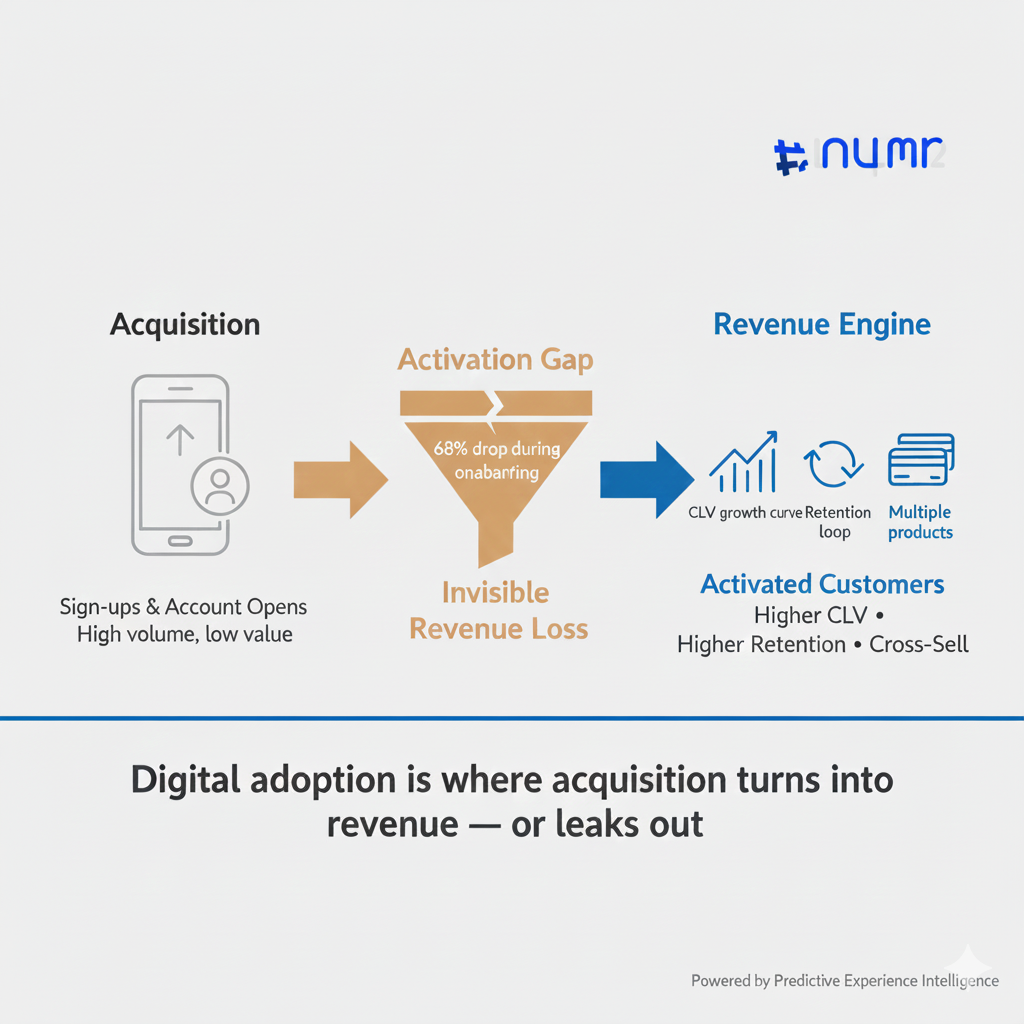

You are facing banking’s greatest paradox: 89% of consumers rely on mobile apps, yet an estimated 68% abandon digital onboarding.

Improving digital product adoption requires moving beyond slick UX and implementing a predictive strategy that uses behavioral signals to intervene, recover lost conversions, and protect the $2.09 trillion digital banking market.

As a retail banking CXO, you’ve won the battle of acquisition, but you are still losing the war on activation. Every customer we acquire but fail to activate is not just a missed opportunity; it’s a wasted investment that erodes our Customer Lifetime Value (CLV).

The numbers clearly illustrate the stakes:

The challenge isn’t data availability - it’s visibility. Most banks already have the data but fail to interpret them as signals or the system to connect them to churn or revenue risk.

“While sentiment analysis has been a useful starting point, helping to gauge customer emotions, the true value lies in the predictive capabilities of AI, anticipating customer needs, streamlining operations, and enabling proactive engagement before issues arise.”

– Craig Crisler, CEO at SupportNinja

This expert insight underlines why simply tracking events isn’t enough; you must predict customer behavior and act on it before adoption breaks happen.

We believe the future belongs to institutions that treat activation as a revenue-critical process, not a technology checklist. This guide shows you how.

The first step in improving adoption is confronting the invisible revenue drain caused by silent churn - a phenomenon that hides in your "active" customer base.

Silent churn occurs when a customer looks good on paper—they signed up for a card or downloaded the app - but has effectively disengaged, meaning your bank holds:

These disengaged customers poison your cross-sell campaigns and LTV models. Your reporting tools are likely blind to this, as they rely on lagging indicators.

This is why we need to shift to the Predictive Experience Intelligence (PXI) system.

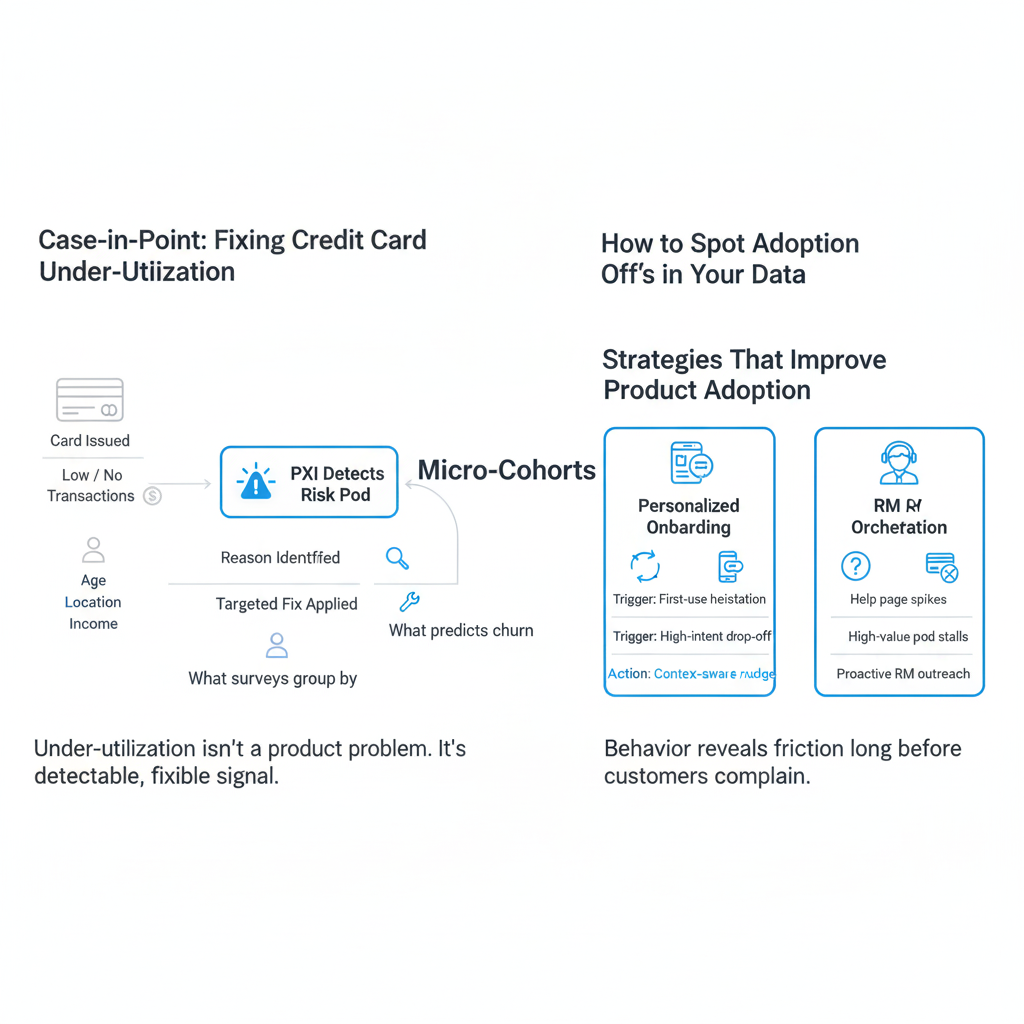

NUMR’s behavioral cohorting identifies these ghosts - and pinpoints what’s blocking activation before they disappear entirely such as unfunded accounts or inactive cards - so you can re-engage or reallocate.

By turning behavioral silence into actionable insight, we bridge the gap between downloaded apps and actively engaged customers.

This is where CX automation for banking becomes essential. Real-time customer insights for banks are only valuable when they trigger immediate, coordinated action, automated nudges for unfunded accounts, contextual in-app prompts for first transactions, or RM alerts for high-value customers showing early disengagement. PXI closes the loop by not just detecting silent churn signals, but by automatically orchestrating the right intervention at the right moment, across digital and human channels. Instead of relying on delayed campaigns or manual follow-ups, banks can systematically convert early friction into activation, transforming real-time insight into automated CX actions that protect revenue and accelerate adoption.

The onboarding process is where the majority of customers - up to 68% - are lost. To fix this, we must move past generic welcome emails and implement progressive, personalized interventions.

Once friction signals are visible, these interventions can be triggered with precision - instead of generic campaigns.

Your focus must be on:

Research shows that 60% of customers would abandon an application if it was too lengthy or cumbersome. Instead of overwhelming customers with every feature at once, we should introduce core functionality immediately and progressively reveal advanced capabilities as the customer demonstrates readiness.

Our goal is to proactively guide customers through friction points using contextual intelligence. PXI detects subtle intent - like a customer repeating a feature peek or abandoning a transactional flow - and triggers immediate, contextual guidance or a Relationship Manager (RM) outreach. This approach:

The true measure of successful adoption is not just retention, but the expansion of your share of wallet. When customers actively use one digital product (e.g., mobile deposits), we gain the trust required to cross-sell additional services.

The data confirms the substantial cross-sell dividend: Customer advocates hold 17% more products with their primary bank compared to non-advocates. These customers allocate significantly more of their financial portfolio to your bank, including:

Our PXI framework strengthens this relationship by identifying where customer relationships are weakening, analyzing the reasons, sending actionable triggers, and thereby automating reactivation, thus protecting this highly valuable CLV.

While digital is the primary access method for 55% of US consumers, your digital strategy must respect the omnichannel reality. Your customers still desire the trust signal of a human safety net: 71% of consumers say in-person access is important, and 68% say phone support is essential.

You must integrate your digital and physical touchpoints seamlessly:

To prove the ROI of your adoption efforts, we must focus on metrics tied to shareholder value, not just vanity scores.

This comprehensive approach allows us to move from reporting "satisfaction" to reporting "retained revenue".

NUMR flags the cohort, identifies the reason for drop-off, and triggers tailored fixes that lift usage.

Micro-cohort analysis (grouping users by shared behavior signals, not just demographics) - look for groups who retry the same step, switch devices, or repeatedly open help pages. These shared behaviors (not demographic labels) are the early warning signs of friction.

Session-level signals, repeated retries, device switching, and transaction errors are all visible in event logs and tell a story that surveys often miss.

Once friction signals are visible, these interventions can be triggered with precision - instead of generic campaigns.

Q: Our app has many features. Is low adoption a product design problem?

While UX complexity is a factor (60% of customers abandon lengthy applications), not necessarily; often it’s a signal of unseen friction in the journey, not dissatisfaction with the product itself. We must use behavioral analytics to prioritize high-impact features and deploy targeted, in-app nudges to guide users, rather than assuming they will find the value on their own.

Q: How quickly can we expect to see ROI from improving digital adoption?

You should expect initial ROI within 6 to 12 months through operational efficiency gains (e.g., reduced call center volume) and quick wins in conversion recovery. Long-term benefits, such as the 17% CLV lift from digital advocates, compound over 18 months.

Q: What is the risk of using AI for personalization and nudging?

The biggest risk is the personalization gap: 72% of customers expect personalization, but only 3% actually use personalized tools. Our PXI approach mitigates this by using AI to analyze customer behavior and intent before sending a nudge, ensuring the message is timely, relevant, and not perceived as intrusive.

Q: How does PXI handle the "silent churn" in new accounts?

PXI detects silent churn by tracking behavioral micro-cohorts - like new customers who complete wealth onboarding but fail to invest. It then automatically triggers an ACTION (an RM alert or an automated recovery message) to re-engage that customer before the relationship decays.

Q: How can we integrate this kind of intelligence with our existing CRM?

Our PXI platform is designed with an API-first approach, enabling modular deployment that integrates seamlessly with your existing CRM, core banking, and contact center systems. We act as an intelligence layer that feeds signals and recommended actions into your current workflow, without requiring a costly system overhaul.

Digital product adoption is the new frontline in the battle for banking revenue. As we have shown, the banks that move quickly to adopt a Predictive Experience Intelligence model - one that sees risk, explains the root cause, and fixes it automatically - are the ones achieving 41% faster revenue growth.

The future belongs to the banks that turn every behavioral signal into a revenue opportunity.

Book your Strategy Session with NUMR. Discover how our predictive experience intelligence system can implement this framework to turn your digital adoption gaps into measurable revenue growth.

.png)

.png)

.png)