CX is now a primary growth engine in banking, yet 50% of executives fail to attribute its value to the bottom line.

Measuring CX ROI requires shifting from reactive feedback management to a PXI (Predictive Experience Intelligence) system that connects behavioral signals to revenue outcomes in real time and triggers fixes.

Banks that excel in customer experience show 41% faster revenue growth compared to their competitors, while customer-obsessed businesses demonstrate 49% faster profit growth.

This post provides the definitive metrics and the PXI™ system for banking leaders to quantify their CX investment.

Customer experience (CX) has evolved beyond a support function in today’s fiercely competitive market. CX is now a strategic determinant of financial performance.

The stakes are clear: 89% of businesses now compete primarily on CX, but there is a profound disconnect - only half of CX decision-makers track their function’s contribution to organizational success. That disconnect exists because legacy systems rely on lagging indicators - surveys, NPS, satisfaction - while PXI brings leading indicators that capture behavioral shifts before revenue is lost. Feedback remains one input—PXI primarily operates on behavioral signals and uses feedback for confirmation, not dependence.

Most banks don’t lose customers.

They lose visibility before it actually happens!

This blind spot is costly.

“Customer Satisfaction (CSAT), NPS and effort scores are good metrics, but there is a need to demonstrate the link to top-line and bottom-line results.”

– Luka Popovac, Head of Customer Experience, McDonald’s

That’s exactly why traditional CX measurement fails to connect to financial outcomes. While satisfaction scores and survey data provide useful context, they rarely explain why experience improvements translate into revenue protection or growth or how much. This is where your PXI framework bridges the gap by tying behavioral signals directly to dollarized outcomes.

Poor customer experience threatens $3.7 trillion of global sales globally in 2024, with 47.3% of banking customers citing poor service as their primary reason for switching institutions.

By contrast, banks that deploy PXI — the predictive experience system that detects early friction signals such as unfunded accounts, repeated disputes, or digital drop-offs - are able to intervene preemptively, directly impacting the P&L statement:

The goal for banking CXOs is no longer to simply raise satisfaction scores, but to establish a robust, objective framework for demonstrating these financial returns.

For many, CX quality is the primary driver of loyalty, with 71% of US banking customers citing it as the main reason they remain loyal to their bank.

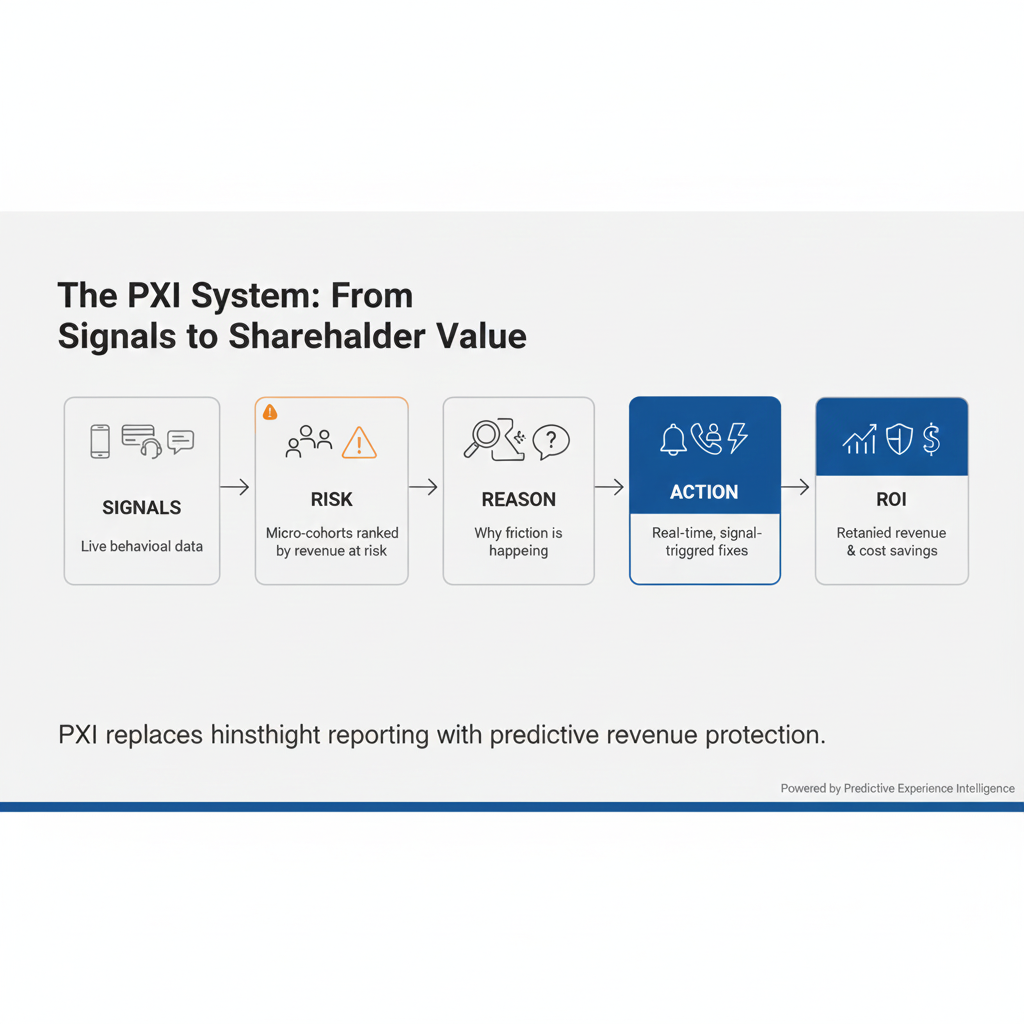

The core challenge in measuring CX ROI isn’t collecting data - it’s connecting it. Most CX programs measure sentiment; few can prove causation. That’s where NUMR’s Predictive Experience Intelligence framework stands apart. PXI shifts CX from reporting to predictive prevention and measurable ROI.

PXI transforms CX measurement from reactive reporting into predictive revenue protection by detecting behavioral signals, correlating them with financial metrics, and triggering automated interventions - proving that a specific CX initiative - like improving digital onboarding or automating service - directly caused a change in a business metric, such as reduced churn or increased cross-sell.

This framework operates on these 5 non-negotiable principles:

To accurately attribute ROI, you need a single, panoramic view of the customer journey.

PXI unifies data across core banking systems to centralize customer interactions across every touchpoint - CRM, call centers, transaction ledgers, chatbots, and app analytics - revealing where friction emerges and how it impacts retention. PXI ingests streaming behavioral events (logins, retries, drop-offs, delays) to catch weak signals as they emerge—not in quarterly reports.

With all signals centralized, PXI eliminates the silo problem that plagues legacy CX stacks. Every customer action becomes measurable, attributable, and linked to financial outcomes.

This unified signal layer is what enables CX automation for banking to operate with precision rather than guesswork. Real-time customer insights for banks are generated the moment these signals occur: failed authentication attempts, repeated balance checks without transactions, or sudden channel switching, and are immediately evaluated for commercial risk. Instead of routing insights into static dashboards, PXI feeds them directly into automated decisioning and orchestration engines, triggering contextual actions across digital, service, and relationship-manager workflows. By acting on signals while the customer is still in the journey, banks move from observing experience breakdowns to automatically correcting them, turning real-time insight into continuous, scalable CX intervention.

Traditional surveys miss the most critical signals - the customer's behavior and silence.

This requires tracking every signal of frustration or disengagement. By continuously monitoring behavioral signals (login retries, card activations, app drop-offs, complaint escalation patterns), PXI detects micro-cohorts at risk of disengagement long before they surface in churn metrics. PXI quantifies exposure (e.g., unfunded accounts worth $XM/mo) and prioritizes cohorts by revenue at risk.

For instance:

This focus on early warning signs allows PXI to anticipate a support need or churn event long before the customer complains or officially closes their account.

The framework moves past simple correlation (e.g., "high satisfaction is often linked to low churn") to establish causation. PXI transforms raw data into revenue intelligence by connecting behavioral patterns with financial consequences.

If a surge in app drop-offs correlates with declining card activations, PXI establishes why by connecting the behavioral pattern with the financial consequence, rather than simply reporting the decline. Insights must identify the who, uncover the why, and provide specific guidance on the next steps. PXI then runs a micro ‘why’ loop: in-app one-tap prompts, targeted RM outreach, or call-transcript mining to confirm the root cause. This blends behavior with just-in-time conversational feedback to explain why the risk exists—before we act.

PXI translates causal insights into real-time alerts and automated workflows that proactively protect revenue.

It initiates the right interventions - such as automated recovery, RM nudges, or workflow alerts - before the relationship decays. Actions are orchestrated to the right system (app, CRM, contact center, branch) with pre-defined playbooks tied to the diagnosed reason.

This means transforming raw data into automated actions that are timely and contextual. For example, if a customer fails to activate a new card three times, PXI escalates immediately to a human RM, or if an app drop-off occurs, PXI triggers an automated recovery message. This turns CX insights from passive dashboards into active levers of revenue protection.

The final stage links the executed ACTION directly back to shareholder value. PXI is built to measure the exact return on investment from the intervention.

It explicitly quantifies the revenue risk prevented, linking the fix (e.g., the RM nudge, the automated workflow) to metrics like:

This process also ensures that CX leaders report retained revenue and cost savings, not just satisfaction scores. PXI A/Bs and benchmarks each intervention to attribute: customers retained, conversions recovered, and cost-to-serve reduced, all per cohort and journey.

These are outcomes PXI quantifies, distinct from the 5-step PXI loop.

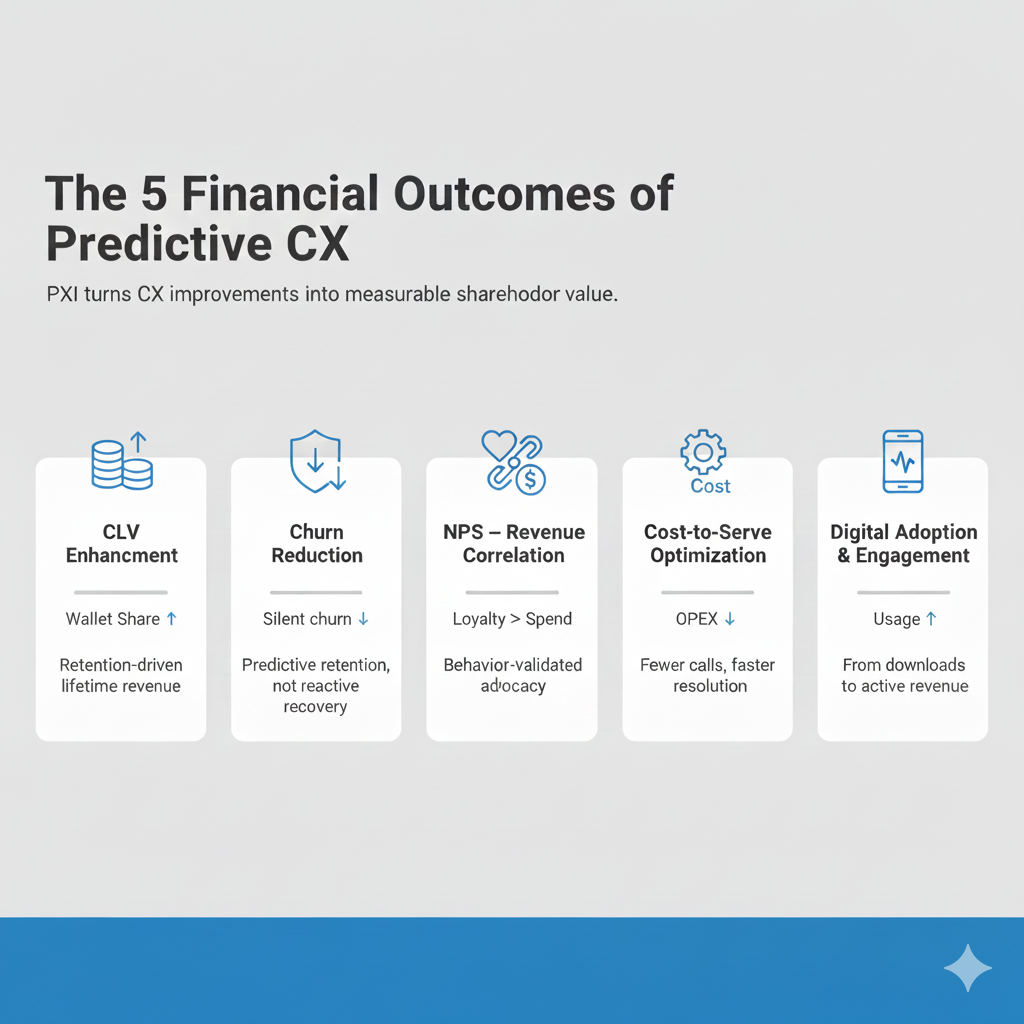

Once the retail banking leaders apply the Predictive Experience Intelligence System, they receive the biggest outcomes in terms of these five primary financial metrics that directly link CX improvements to shareholder value.

CLV represents the total revenue a customer is expected to generate throughout their entire relationship with the bank.

Improved CX drives CLV through increased wallet share and longer retention. PXI strengthens CLV by identifying where customer relationships are weakening - unfunded accounts, inactive cards, or low engagement segments - and automating reactivation.

Customer advocates identified early through PXI are highly valuable, holding 17% more products with their primary bank compared to non-advocates.

They allocate significantly more of their wallet share, including +5% more on savings accounts, +12% more on personal loans, +18% more on investments, and +30% more on insurance products.

Key CLV Calculation Components:

By using PXI to track retention-linked behaviors instead of generic satisfaction, banks can lift CLV with precision.

Since acquisition costs far exceed retention costs, reducing churn provides immediate and measurable ROI. Retention strategies are becoming paramount, with banking leaders increasing focus on customer engagement strategies from 17% to 21% as a top priority in 2025.

And you have to understand that retention is no longer a static KPI; it’s a predictive signal model. PXI maps the likelihood of churn by analyzing patterns of disengagement before customers formally leave.

The reward for delivering exceptional CX is high retention: banks scoring above 85% in CX satisfaction surveys maintain 2.4x higher retention rates than their lower-performing peers.

Banks using PXI for early churn prediction report:

Key Retention Metrics to Track:

Retention metrics become not just retrospective - they become forecastable.

NPS alone is a vanity metric, but when accurately correlated with financial results, it becomes a powerful predictive tool. PXI de-emphasizes NPS as a driver; it overlays NPS where available to triangulate with behavior and spend.

It connects NPS fluctuations with behavioral outcomes - like transaction volumes, app usage, and cross-sell activity. When NPS rises but transactions fall, PXI identifies the mismatch, ensuring banks measure real loyalty, not perceived satisfaction.

In fact, 82% of respondents identify CX as the leading driver behind customer loyalty, positioning it as the most critical factor for banking executives to address.

Banks must connect NPS improvements to tangible outcomes such as:

This behavioral overlay transforms NPS into a forward-looking revenue indicator.

A superior customer experience often lowers operational costs, turning CX into a cost-saving tool.

This is particularly crucial as retail banks face pressure on Net Interest Income (NII).

Improved CX in the branch channel dramatically reduces friction: when banks deliver on basic customer service fundamentals (welcoming customers, fast service, using names), branch satisfaction scores increase by 123 points compared to average performance.

Furthermore, 64% of banking consumers still rely on branches for conflict resolution, and 65% see branches as symbols of stability across all generational segments. PXI preempts service spikes (e.g., login-failure bursts) with auto-alerts and self-service fixes, turning CX into a predictive OPEX advantage.

CX improvements reduce operational friction, leading to:

How does PXI rescue the day here?

Well, PXI enhances cost efficiency by pre-empting service spikes.

For example, it detects anomalies like a surge in login failures before they flood the call center, automatically triggering alerts or self-service fixes.

This intelligence reduces:

PXI essentially converts service cost reduction into a predictive OPEX advantage.

Digital channel migration is a major source of cost savings and satisfaction; for instance, 42% of U.S. consumers prefer using a mobile app to manage finances.

While mobile apps generate an average of 150 interactions per customer annually, banks face a significant personalization gap.

Although 72% of customers say personalization influences their bank choice, only 3% actually use personalized tools offered by their banks. This disconnect is further exacerbated by the knowledge gap, where 60% of banking customers expect their banks to understand their specific needs, yet ONLY 53% of customers don't even know their own savings interest rate.

Banks should measure the ROI from:

When it comes to PXI, it personalizes digital journeys by tracking contextual signals (session frequency, feature drop-offs, repeat actions). PXI detects intent (repeat feature peeks, abandoned flows) and triggers contextual guidance or RM outreach to convert exploration into usage.

It recognizes, for instance, when a customer explores investment options but never completes a transaction - prompting the right in-app guidance or RM outreach.

This leads to:

By turning behavioral silence into actionable insight, PXI bridges the gap between downloaded apps and active customers.

While the general formula for CX ROI is (Financial Benefits – Cost of CX Investment) / Cost of CX Investment × 100, banking requires tangible, real-world examples.

Scenario: A bank invests $500,000 in a PXI-powered agent assistance system that uses behavioral pattern detection to guide responses in real time.

PXI identified the upstream friction before calls surged, then agent-assist reduced AHT by 40s. The bigger ROI is prevented volume plus efficiency.

Hence, the system reduces Average Handle Time (AHT) by 40 seconds across 4 million annual calls, with agent costs at $25/hour.

Calculation of Financial Benefit (Cost Reduction):

Final CX ROI:

Beyond time savings, PXI quantifies prevented loss—averted contacts, retained customers, and recovered conversions.

PXI shifts ROI measurement from efficiency gains to foresight gains.

This example demonstrates how a strategic CX investment in PXI™ simultaneously drives operational efficiency and improves the customer experience, leading to compound returns because you now have the predictive capability of what drives financial benefits in your operations.

The most common mistake is focusing exclusively on lagging indicators (like NPS or CSAT) without establishing clear attribution to financial outcomes.

This leaves CX leaders reporting "satisfaction" instead of "retained revenue." The solution is implementing leading indicators (like digital engagement, effort scores) and lagging indicators (like revenue growth and churn reduction) simultaneously.

Implement the NUMR PXI framework.

This involves deploying control groups when rolling out new CX initiatives, allowing you to compare performance between the test and control segments to isolate the true impact of the changes on business outcomes. Where RCTs aren’t possible, PXI uses look-alike cohorts and pre/post baselines for defensible attribution.

No. While digital channel migration is a key ROI driver, the most advanced frameworks (like NUMR's) connect all channels - digital, call center, and branch - to create a unified view. This is crucial as 71% of consumers still say in-person access is important, and 68% consider phone support essential.

Digital-only banks, for instance, demonstrate the power of efficient, integrated CX with superior performance, achieving just 10.8% customer churn rates compared to the global average banking retention rate of 82.4%.

Predictive prevention — PXI tracks Signals → Risk → Reason → Action → ROI to quantify prevented loss, not just realized gain. It is not just about realized gain. Every averted churn, early reactivation, or prevented service escalation translates to measurable retained revenue.

Yes. PXI integrates seamlessly with CRM, core banking, contact center, and digital analytics platforms through API-based modular deployment - enabling predictive analytics without disrupting IT infrastructure.

Absolutely. NUMR’s PXI framework uses tokenization, audit trails, and hybrid deployment (on-prem or cloud) to ensure data sovereignty and full compliance.

The business case for investing in customer experience is no longer a matter of faith; it is a matter of demonstrable financial returns. From TSB Bank achieving an 86% improvement in first-response time to banks seeing 10-15% revenue growth, the proof is in the numbers.

The future belongs to the banks that adopt a Predictive Experience Intelligence (PXI)—the only system that sees risk, explains it, and fixes it before revenue fades.

But without PXI, most banks are still measuring hindsight instead of managing foresight.

PXI completes the shift from descriptive CX analytics to Predictive Experience Intelligence - the ONLY future-ready system that sees risk, explains it, and fixes it before your revenue fades.

Book your Strategy Session with NUMR and Witness PXI™ in action.

Discover how our predictive experience intelligence platform can implement this PXI™ framework to quantify CX ROI and turn experience improvements into measurable revenue growth.

.png)

.png)

.png)