TL;DR

Selecting the right Customer Journey Analytics (CJA) platform is the most critical investment your bank will make this year.

With 89% of businesses now competing on experience, relying on legacy survey tools is no longer tenable.

Most traditional customer journey analytics tools tell you what happened. The next generation predicts what will.

Your analytics should stop reporting what you lost. They should forecast what you will lose and stop it. This guide provides a direct comparison of the top platforms, highlighting the one that moves beyond dashboards to deliver predictive experience intelligence (PXI) - the definitive requirement for any banking CX leader in 2025.

When it comes to retail banking leaders across the globe, your ability to connect customer experience improvements directly to revenue is the single greatest competitive advantage.

Banks that excel in CX show 41% faster revenue growth compared to their competitors, and a single-point improvement in the CX Index can generate an additional $7.93 in annual revenue per customer.

Yet, despite these undeniable financial stakes, you face a fundamental measurement gap.

That gap is most visible in the banking customer experience itself. While banks collect vast amounts of interaction data across digital, branch, and contact-center touchpoints, very little of it translates into real-time customer insights for banks. Experience signals arrive too late, too aggregated, or too disconnected from revenue outcomes to influence decisions while they still matter. As a result, CX teams are left explaining churn after it happens, rather than identifying experience friction as it emerges and intervening in-flight. In a market where switching costs are falling, and digital-first leaders set expectations, the inability to operationalize real-time banking customer experience insights is no longer an analytics issue; it is a direct threat to growth, retention, and lifetime value.

These are the factors that every CFO holds dear to themselves.

This is the near-term cash the business stands to lose if a high-value pod continues to stall - not a percentage or score. Dollars-at-risk is calculated by mapping the pod (e.g., unfunded wealth accounts, stalled loan completions) to the expected transaction value, conversion probability, and time window.

A CFO wants a ranked list of pods by $ exposure, so priorities are commercial (save the biggest dollars first). PXI produces that list by scoring pods for probability × expected value and updating it in real time as signals change.

Customer Lifetime Value is the long game: small frictions today compound into materially lower wallet share, and fewer cross-sells over the years. CLV impact is modeled by projecting how interventions (or failures to intervene) change retention, product holding and spend over time.

For the finance team, the question is: “If we recover X% of this pod now, how does CLV move?” PXI lets you model that by turning recovered conversions and re-engagement lifts into incremental lifetime revenue - making CX spend a defensible investment against future revenue.

This is the operational savings from preventing high-cost service events (contact spikes, repeat calls, manual escalations). Rather than measuring service after the fact, CFOs want the delta: fewer calls, lower AHT, and fewer escalations translated into dollars saved.

PXI reduces cost-to-serve by preempting issues (self-service fixes, targeted nudges, automated RM outreach) and by ensuring first-time fixes - both reduce headcount pressure and lower per-ticket cost. The finance metric is simple: baseline OPEX for a journey vs. OPEX after PXI interventions = predictable cost savings you can budget and scale.

Traditional customer journey analytics tools simply fall short of the demands of modern banking executives because surveys capture only a fraction of the experience, lack clear ROI quantification, and are reactive rather than predictive.

“AI-driven predictive analytics will reshape customer experience in 2025, helping contact centers anticipate customer needs, external factors, and take proactive actions more accurately. This shift will keep leaders a step ahead, foreseeing issues before they arise and creating seamless, predictive customer journeys.”

– Chhandak Biswas, Practice Director, Everest Group

This perspective underscores why banks must move beyond legacy tools toward platforms that predict behavior and automate actions, a core promise of predictive experience intelligence (PXI) for banking.

Your challenge isn't data volume; it’s data quality and actionability. Traditional CX approaches simply fall short of the demands of modern banking executives because:

Legacy analytics trap banks in hindsight - dashboards that catalogue drop-offs but don’t stop them. To close this gap, your focus must shift to platforms that not only have real-time integration of data, but can also apply them to apprehend the problems and fix them before they occur.

PXI flips the script: it reads live signals, ranks commercial risk (Pods), fires automated action, and quantifies the ROI that follows with this simple workflow: Signal → Risk → Action → ROI.

This is where modern banking customer experience strategy breaks from legacy CX analytics. Real-time customer insights for banks are not about faster dashboards they are about interpreting behavioral signals as financial risk while the customer is still active in the journey. Missed payments, repeated authentication failures, abandoned digital applications, or sudden channel switching are not isolated CX issues; they are early indicators of churn, attrition, and revenue leakage. Without a system that continuously connects these live experience signals to commercial outcomes, banks remain reactive, addressing dissatisfaction after trust has already eroded. PXI operationalizes banking customer experience by transforming live behavioral data into prioritized, revenue-linked actions, allowing CX, product, and operations teams to intervene at the exact moment value is at risk.

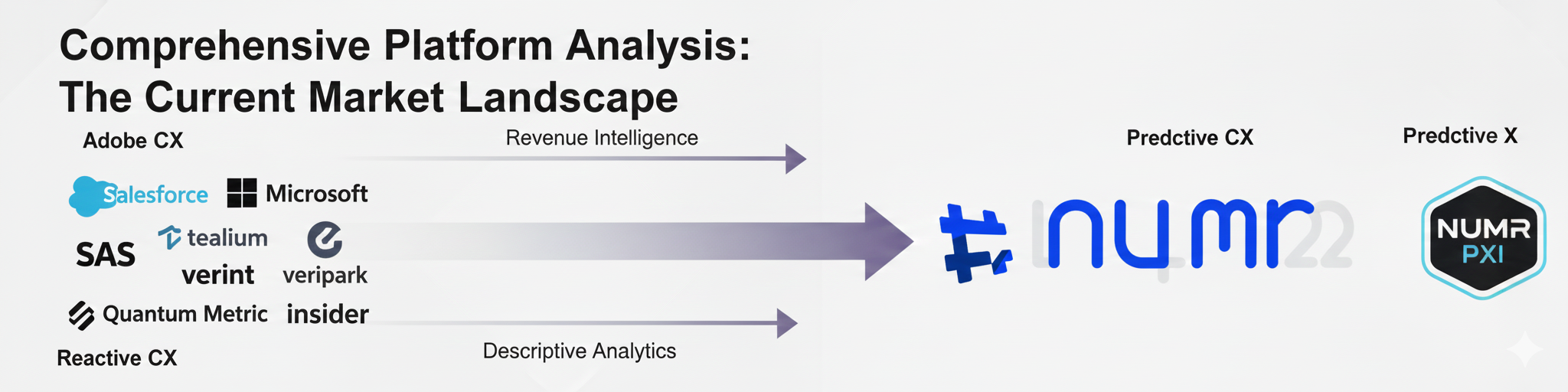

As you evaluate your options for a modern CJA platform, you must look for solutions that combine data unification, predictive intelligence, and industry-specific compliance. Here is a breakdown of the leading contenders in the market.

PXI isn’t another analytics dashboard; it is a forecasting engine for CX risk.

NUMR PXI is the only platform specifically engineered to address the challenges that plague banking CX measurement and its connection to business outcomes in legacy banks. Its core value proposition is connecting CX initiatives directly to revenue outcomes, solving the critical problem of demonstrating ROI.

Core Banking Differentiators:

PXI gap for others: Most vendors detect and orchestrate - NUMR pairs detection with an internal-knowledge-driven fix library and native attribution.

Adobe excels in delivering comprehensive omnichannel experience orchestration, ideal for large banking institutions with complex, multi-channel requirements.

PXI gap: Excellent for omni-channel orchestration, but still relies on observed behavior and not predicted risk. It lacks a plug-and-play, pod-level fix intelligence that automatically maps friction to proven internal fixes.

If your bank is already heavily invested in the Salesforce ecosystem, Journey Builder provides seamless integration with Salesforce Financial Services Cloud.

PXI gap: Strong campaign automation; weaker at extracting reasons from call transcripts and SOPs that could apprehend problems and solve them to positively impact ROI.

Microsoft's platform offers deep integration with existing Microsoft banking solutions and robust compliance features.

PXI gap: Compliance-first; requires additional fix-intelligence layers for pod-driven automation and fixing of silent revenue problems.

SAS offers sophisticated statistical modeling and predictive capabilities, highly valuable for banks requiring advanced quantitative analysis.

PXI gap: Powerful modeling but often lacks the closed-loop operational workflows that map models to automated fixes.

Tealium specializes in data governance and regulatory compliance, making it suitable for banks operating in heavily regulated environments.

PXI gap: Strong governance; lacks predictive fix-intelligence tying pods to proven fixes and attribution.

7. Verint - The Contact-Center & Engagement Specialist

Verint is known for enterprise contact-center analytics, speech and interaction analytics, and workforce optimization - all built to improve agent outcomes and service consistency.

PXI gap: Strong at engagement analytics and agent enablement; lacks PXI’s pod-level predictive triggers and the internal-knowledge fix library that automatically maps recurring contact center friction to proven fixes and dollarized ROI.

Veripark delivers modular digital banking and customer-experience solutions tailored to financial institutions, including onboarding, digital forms, and customer lifecycle tools.

PXI gap: Excellent for standardizing digital journeys and compliance; less focused on cross-channel behavioral micro-signals, pod clustering, and automated fix intelligence tied to revenue attribution.

Quantum Metric surfaces UX friction through session replay, funnel analysis, and continuous product analytics so teams can prioritize high-impact product fixes.

PXI gap: Valuable for surfacing session-level friction; it typically stops short of clustering those frictions into revenue-prioritized pods and automating operational fixes that are proven to deliver boardroom-grade ROI.

Insider specializes in AI-driven personalization and cross-channel orchestration, enabling highly targeted, behaviorally triggered marketing and in-app experiences.

PXI gap: Strong at individualized personalization and orchestration; does not natively perform PXI’s pod-level revenue scoring nor provide the closed-loop fix intelligence that maps operational actions to prevent revenue loss and quantified ROI.

Before you sign any contract, you need to ensure your chosen platform meets the modern demands of banking CX.

This is your most critical factor as revenue attribution will replace NPS as core CX metric. Your platform must provide clear linkage between customer experience improvements and hard financial metrics such as:

The global CJA for Banking market is rapidly growing, projected to reach $24.9 billion by 2033. Your platform must integrate seamlessly with core banking systems, CRM, and risk management systems, not just generic web analytics.

With the growth of banking and transactions, there is a massive upsurge of global fraud. And hence, your bank will be a prime target for such bad actors. Look for platforms that guarantee:

The future of CX is predictive, not reactive. Your platform must leverage AI to:

Modern banks will go digital-first and will be handling massive transaction volumes. You need a solution that can handle the same load. Ensure the platform can provide real-time analytics at scale and support your growing data requirements.

Q: How can I prove the ROI of a new CJA platform to my CFO?

Your focus should shift from reporting CSAT/NPS scores to tracking business outcomes like revenue recovered from drop-offs, cost reduction from reduced call volume, and retention uplift. The NUMR PXI framework is specifically designed to provide this direct financial attribution.

Q: Is CJA only for digital channels like mobile banking?

No. While mobile apps generate an average of 150 interactions per customer annually, your customers still rely on human channels. The most advanced platforms unify digital, call center, and branch data, crucial since 71% of consumers still say in-person access is important.

Q: How does a CJA platform avoid the "data silo" problem we already face?

The right platform, like NUMR PXI, uses an API-first approach to sit on top of your existing systems (CRM, core banking) and pull data into one unified view. This prevents the need for messy data migration and centralizes all your customer signals.

Q: Our bank already uses a survey tool. Can we integrate that?

Yes. Modern, intelligence-first platforms are designed to ingest data from existing legacy CX stacks (like Qualtrics or Medallia). Your new CJA system should act as the intelligence layer, taking raw feedback and combining it with behavioral data to find the root cause and automate the fix.

Q: How long does it take to see a measurable ROI after implementation?

While large-scale CLV improvements are long-term, you can expect to see early ROI almost immediately through operational efficiency gains, such as reduced Average Handle Time (AHT) in your contact center and quick recovery of digital drop-offs, which directly saves money.

The choice of your Customer Journey Analytics platform is a reflection of your bank's strategic commitment to growth and retention. With customer advocates holding 17% more products with their primary bank and banks with the highest advocacy scores growing revenue 1.7x faster, the investment is a necessity.

The key is selecting the solution that transforms your data from a passive report into a predictive asset.

Book a forecast session with NUMR - see how PXI turns customer signals into revenue success.

We will show you exactly how the PXI framework quantifies your revenue leaks and enables your team to fix them automatically.

.png)

.png)

.png)